Ganesh Consumer Q3 FY26 Results: PAT Up 57%, Steady Growth Guidance

Guidance of 15-20% revenue CAGR for FY26-29. After a flat 9M FY26 with expanding margin the forward outlook is not discounted - trading at attractive valuations

1. FMCG Company —

ganeshconsumer.com | NSE: GANESHCP

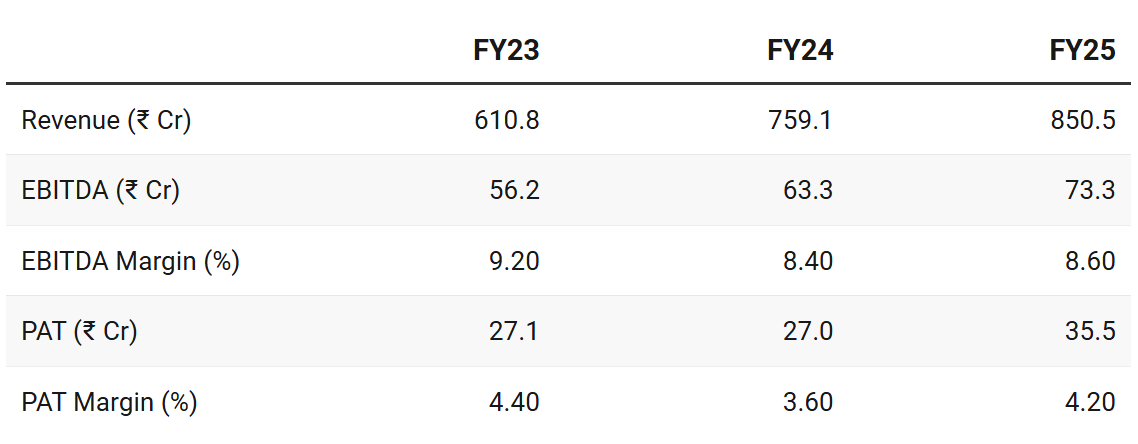

2. FY23–25: PAT CAGR of 15% & Revenue CAGR of 18%

Average performance - nothing spectacular in the past

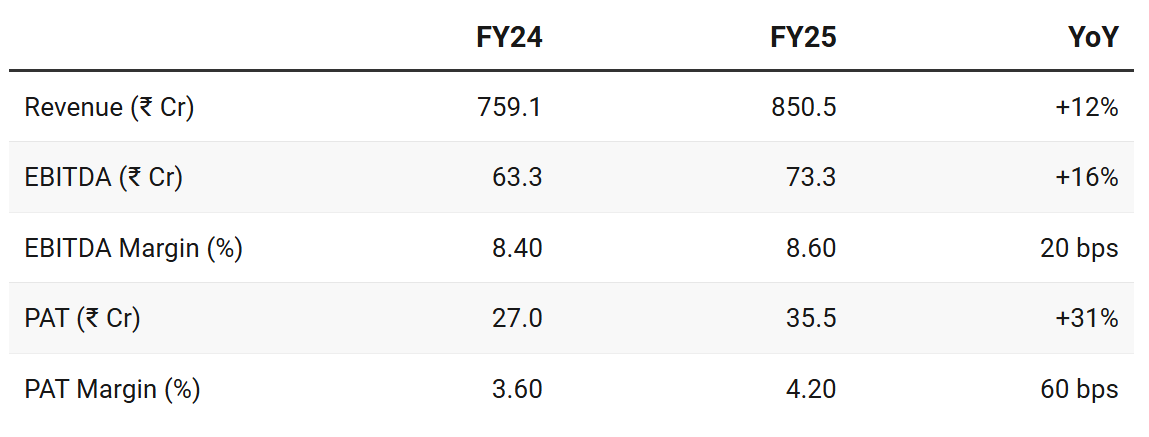

3. FY25: PAT up 31% & Revenue up 12%

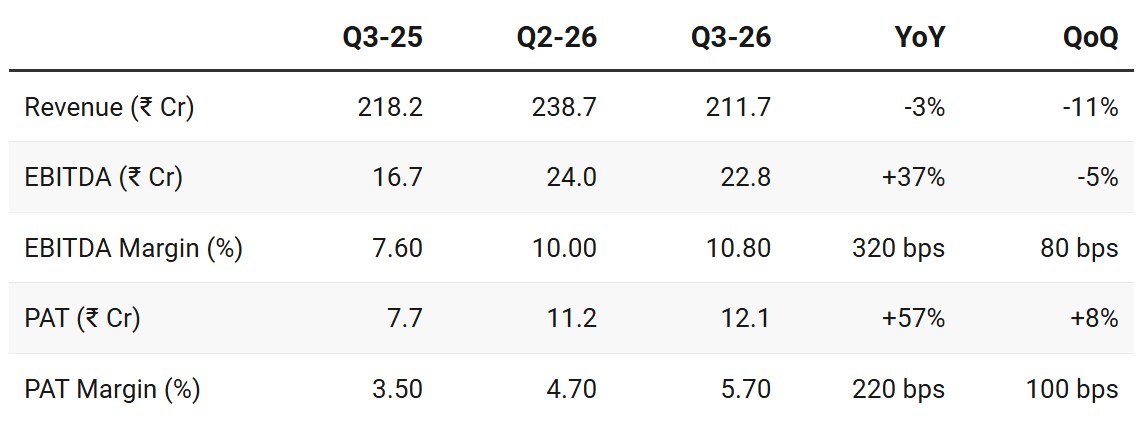

4. Q3-26: PAT up 57% & Revenue down 3% YoY

PAT up 8% & Revenue down 11% QoQ

Revenue dip was a deliberate management decision to scale back low-margin B2B volumes.

B2B revenues declined ~12% YoY.

B2C volumes remained broadly stable (up ~1% in some categories) despite intense competitive intensity. This focus on B2C was the primary driver behind the lift in margins

Q3 saw increased competition in the Eastern market, from Emami entering the staples category (Atta, Maida, Suji) with aggressive pricing.

Rather than engaging in a destructive price war that would erode margins, Ganesh focused on brand recall and its deep distribution network (3.5 lakh touchpoints) — protected its market share in West Bengal while delivering record-high quarterly margins.

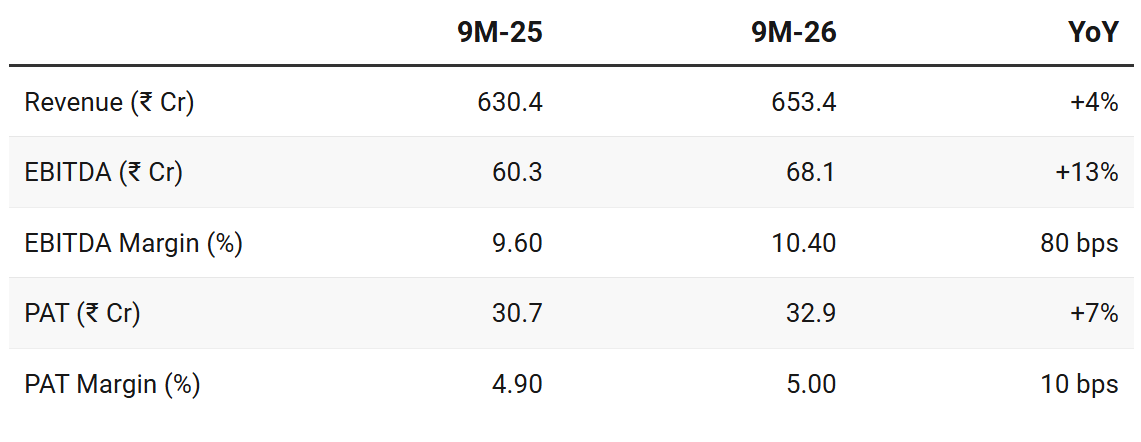

5. Flat 9M-26: PAT up 7% & Revenue up 4% YoY

9M performance highlights the strength of the core and emerging categories:

Atta (Core Base Category): Delivered strong 13% volume growth.

Atta serves as the “carrier product” that drives distribution for other high-margin items.

Overall B2C Volume: Revenue from the B2C segment grew ~5% in volume and ~6% in value.

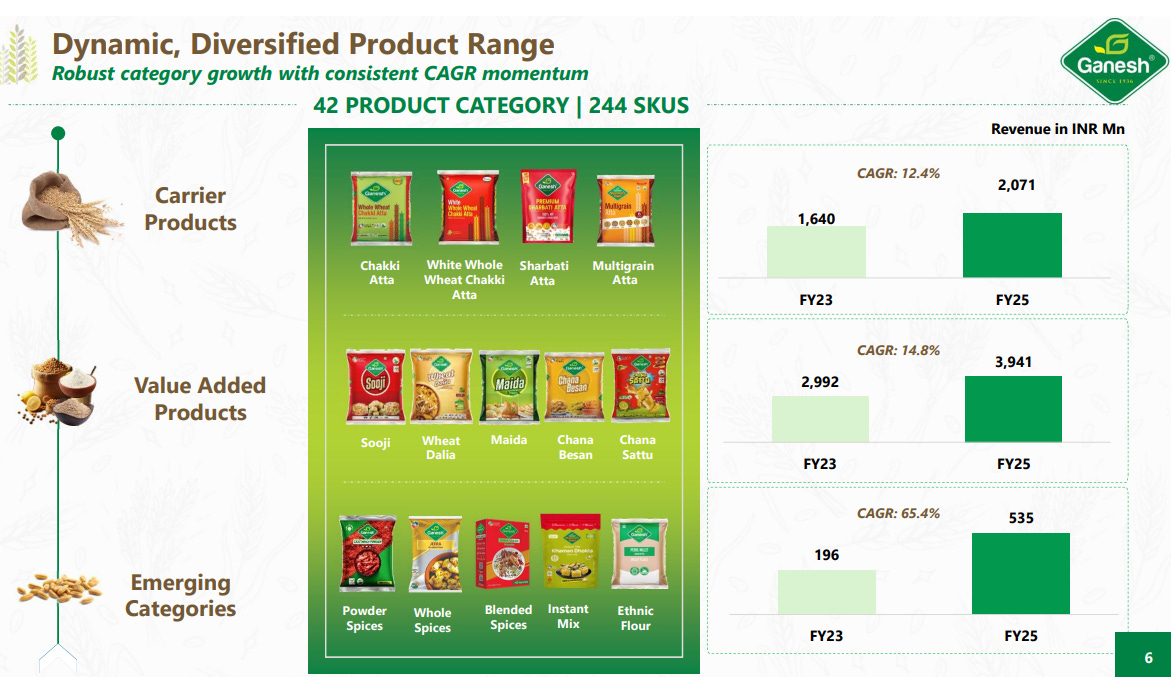

Spices Growth: “Emerging” spices category grew nearly 31% YoY, confirming it as the primary long-term margin accretive driver.

Quick Commerce & E-commerce: Grew by 58% YoY over the 9M period, indicating a successful shift in consumer purchasing behavior and effective digital marketing.

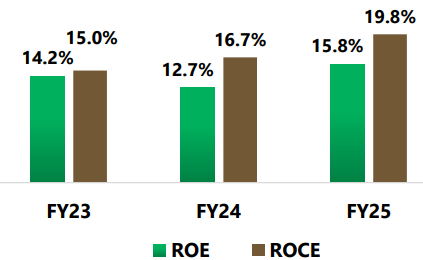

6. Return Metrics: Improving Return Ratios

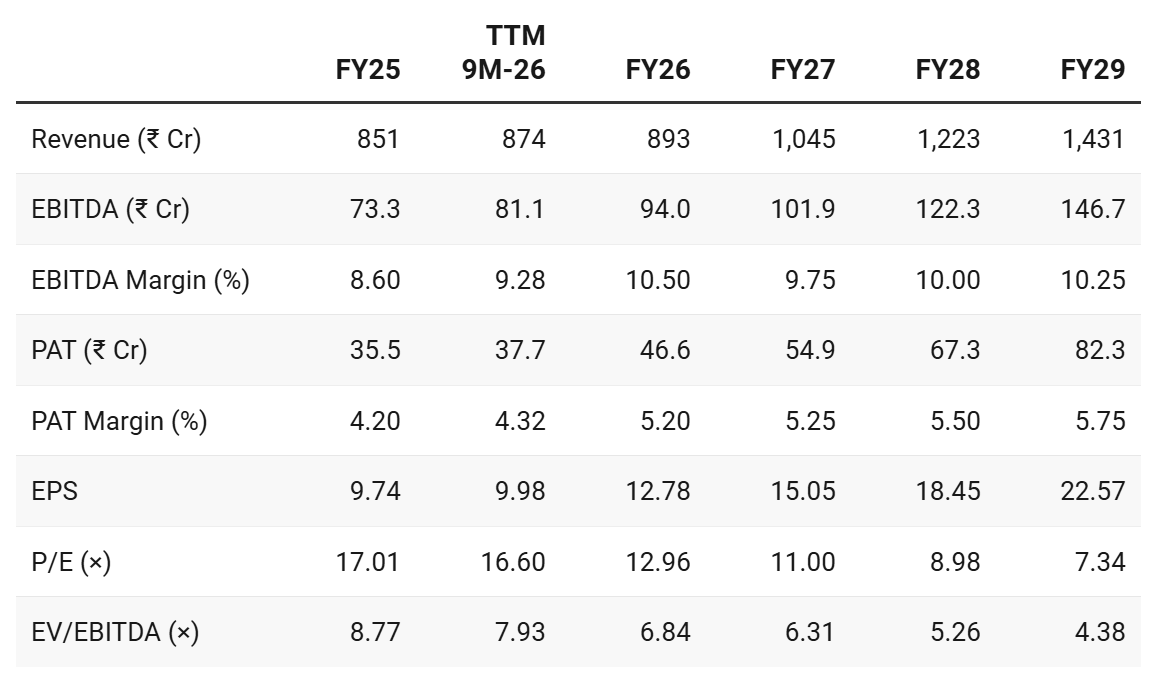

7. Outlook: 15-20% Revenue CAGR for FY26-29

7.1 Management Guidance

Guidance for 15-20% growth till FY29 — strong turnaround from a flattish FY26

FY26 Guidance: We feel that there'll be a single digit growth on the entire year. Yes but Q4 specifically as I said in the January month we have delivered better volume growth, so we feel that in the entire quarter 4, there'll be a higher single digit volume growth

FY29 Revenue Target: Management believes they have the headroom to reach a revenue of ₹1,400-1,450 Cr within the next three years by increasing capacity utilization from the current 55-57% to 85%.

And going forward, we will maintain a growth rate of around 15% to 20% on the revenue side. And on the EBITDA side, we feel that anywhere between 9.5% to 11% we’ll be able to deliver.

7.2 9M FY26 Performance vs FY26 Guidance

Guidance at end of Q2-26: So we feel that we’ll be able to have an annual growth rate of 12% to 15% this year.

Guidance at end of Q3-26: We feel that there’ll be a single digit growth on the entire year.

Overall performance has been weak — growth guidance has been slashed.

Q4 saw a January Rebound: The “B2B reset” of Q3 began to pay off in January, which saw a ~9% volume growth in B2C.

However the weakness is restricted to FY26

The 15-20% revenue CAGR target intact till FY29 with a revenue target of ₹1,400-1,450 Cr

Margin performance has been strong despite the weak top-line growth

8. Valuation Analysis — Ganesh Consumer Products

8.1 Valuation Snapshot

Current Market Price: ₹165.65; Market Cap: ₹669.4 Cr

Valuations based on 17% growth rate in line with the 15-20% growth guidance.

Valuations are attractive from an FY26 perspective.

20% of the market cap of GANESHCP is in cash — provides a safety cushion to the valuations

However the management intent of rewarding shareholders through dividends or buybacks is a big red flag — the management at scale of less than ₹1,000 Cr market cap does not have ideas to deploy the cash as growth capital.

Cash Reserves: ₹130-135 Cr in bank balances and is evaluating rewarding shareholders through dividends (target payout >20-25%) or buybacks.

Opportunity of re-rating of multiples if growth guidance is delivered

8.2 Opportunity at Current Valuation

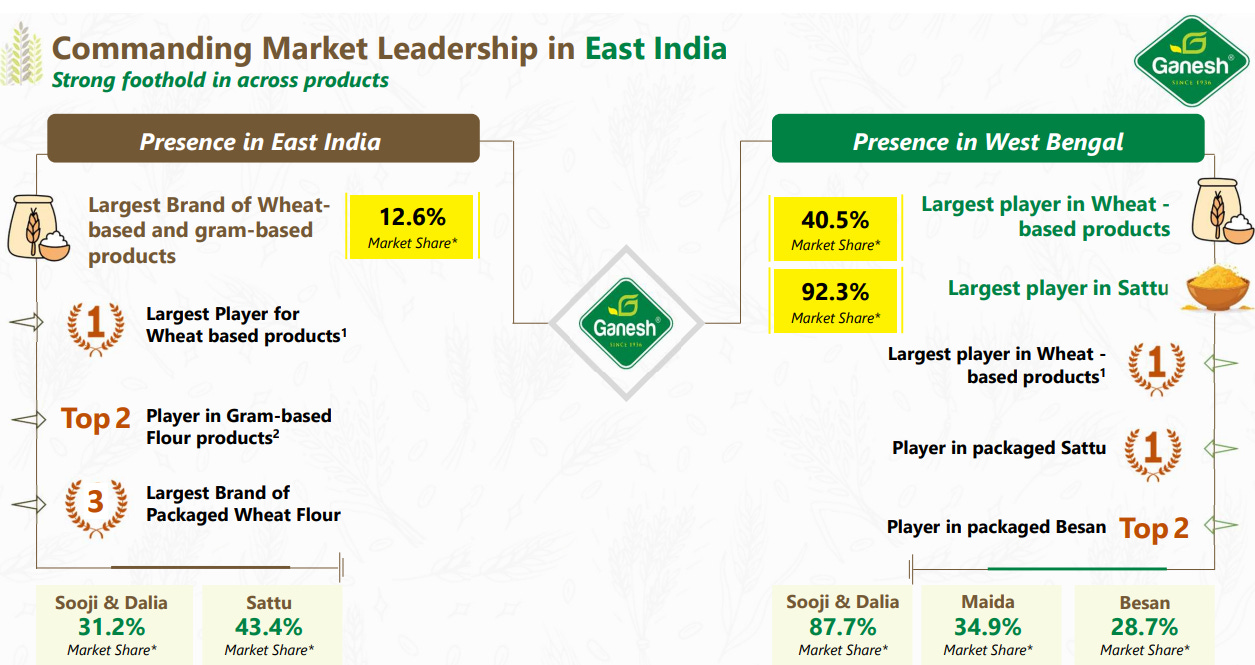

Unorganized to Branded Shift: In West Bengal, 82% of wheat and gram derivatives are still sold in loose.

As consumers move towards brands, Ganesh—as a local leader—is best positioned to capture this conversion.

Dominant Market Share in Core Hub: Ganesh holds a commanding position in its home market of West Bengal — this provides a stable “cash cow” to fund expansion into new territories.

High-Margin Product Pivot (Spices): Management is aggressively pushing into the Spices segment which offer significantly higher gross margins compared to basic flours. Success here could lead to a permanent rerating of the company’s overall margin profile.

Geographic Expansion (The “Next Bengal”): The company is replicating its West Bengal success in Bihar, Jharkhand, Odisha, and the Northeast. Early signs are positive, with Bihar showing 36% growth in a single quarter. The new Agra and Varanasi units provide the logistical “near-to-farm” advantage needed to serve these states profitably.

The hurdle for success is low — for the investment thesis to play out the required run-rate is 15-20% which looks reasonable considering the base of GANESHCP.

Additionally valuations are not demanding allowing for a margin of error in the growth projections.

8.3 Risk at Current Valuation

GANESHCP did not deliver on its original FY26 guidance — what if the trend continues forward.

Intense Competition: Ganesh faces a two-sided battle:

National Competitors like ITC (Aashirvaad), Adani Wilmar (Fortune), and Patanjali have massive marketing budgets.

New Regional Entrants: Entry of Emami into the staples category led to a “price war” in Q3 FY26, which forced Ganesh into a “tactical reset” and slowed its revenue growth.

Geographic Concentration: Despite expansion efforts, ~93% of B2C revenue still comes from West Bengal. Any regional economic slowdown, regulatory change, or intense local competition in that single state could disproportionately impact the company’s entire performance.

Commodity Price Volatility: As a staples business, the company is highly sensitive to the prices of wheat and gram. While they have a strategic inventory-buying policy, a prolonged spike in raw material costs can squeeze margins, as seen in the previous fiscal year (H2 FY25).

Seasonality Risk: High-margin products like Sattu are heavily weather-dependent. A shorter-than-expected summer (as in Q2-25) can lead to significant revenue misses in those specific categories.

Execution Risk in New Markets: Building brand trust in states like Bihar and Odisha requires significant upfront investment in distribution and marketing. There is no guarantee that the “Ganesh” brand will have the same pull in these regions as it does in Bengal.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer