Frontier Springs Q2 FY26 Results: PAT Up 24%, On-track FY27 Guidance

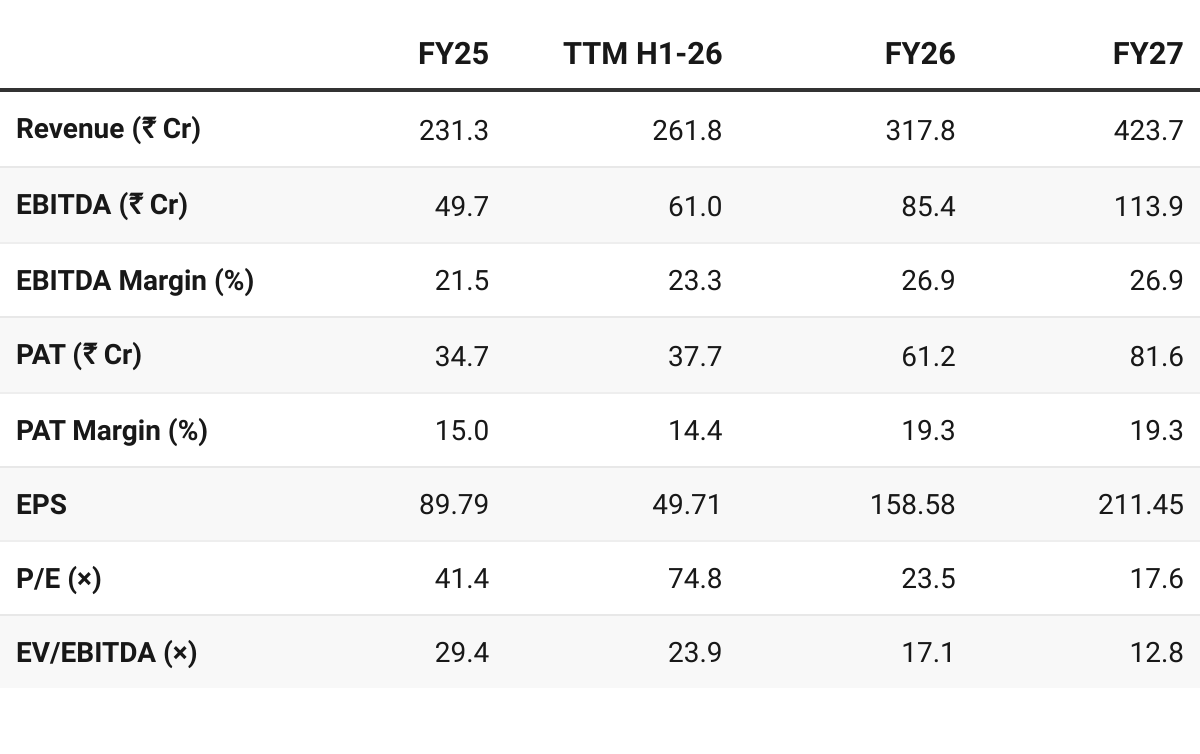

Revenue CAGR of 35% for FY25-27 with strong margins. After a strong Q2 FY26 Frontier Spring available at reasonable valuations based on FY27 forward valuations

1. Supplying springs and forgings for Indian Railways

frontiersprings.co.in | BOM: 522195

The company primarily produces Hot Coiled Compression Springs and forging items, catering especially to the needs of Wagon, Locomotives, and Carriage sectors. Registered with RDSO since 1990, Frontier Springs is a trusted supplier to the Indian Railways

Indian Railways – Our Primary Customer

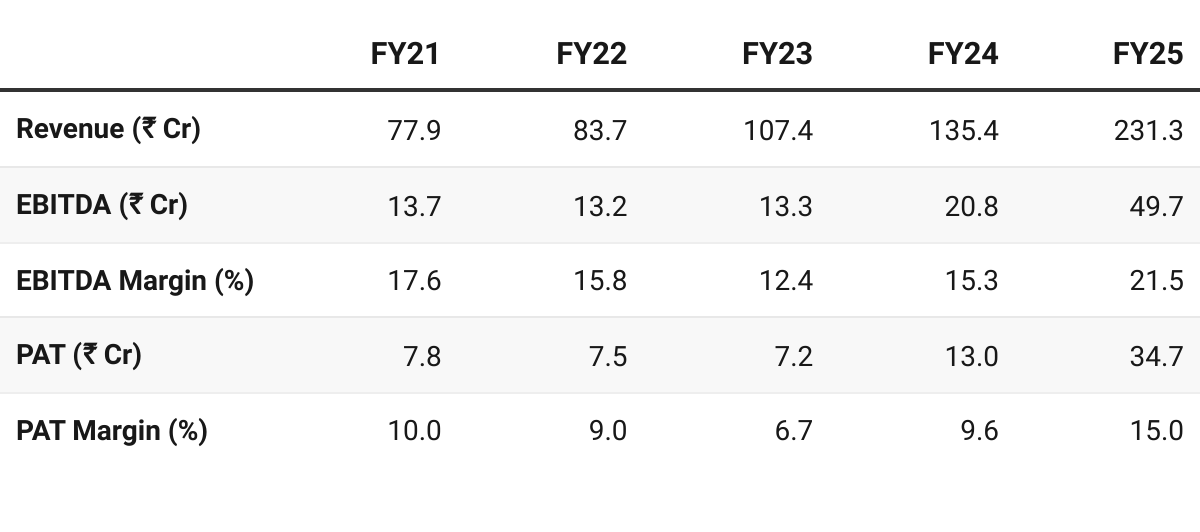

2. FY21–25: PAT CAGR 45% & Revenue CAGR 31%

3. FY25: PAT up 167% & Revenue up 71% YoY

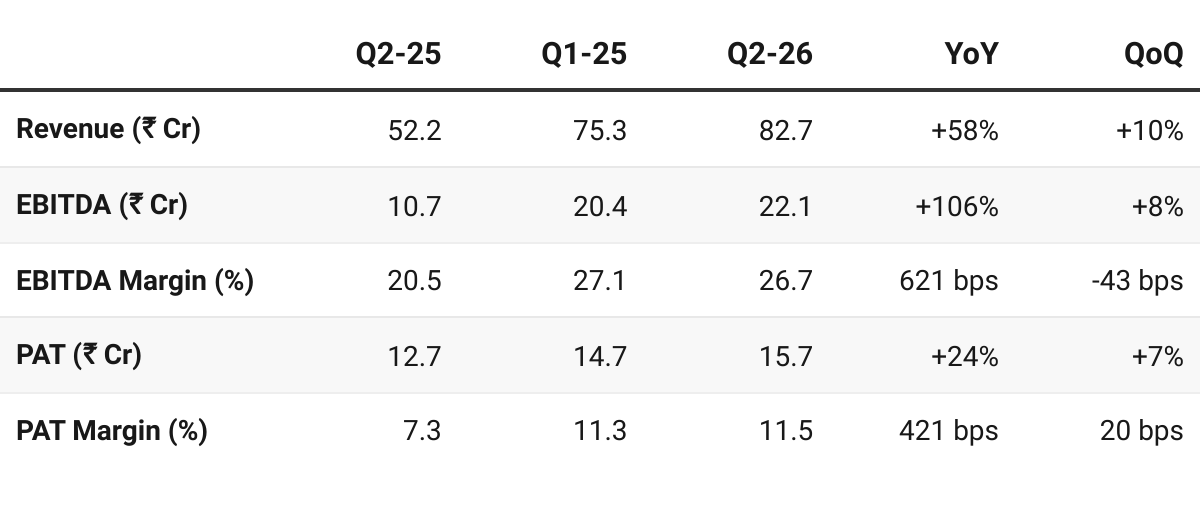

4. Q2-26: PAT up 24% & Revenue up 58% YoY

PAT up 7% & Revenue up 10% QoQ

Strongest quarterly revenue

Growth broad-based across Coil Springs, Air Springs and Forging.

Margins expanded sharply due to:

Better pricing to Indian Railways because of tight supply

Higher Air Spring contribution (structurally high-margin)

Forging utilization improving

Operating leverage from higher volumes

Air Springs (High Margin) — ₹35–40 Cr

Demand extremely strong — ~40% market share

Railways shifting to air springs for secondary suspension across VB trains, Metros, and LHB.

Continental Germany partnership continues to be a competitive moat.

Coil Springs — ₹35–40 Cr

Stable demand from Indian Railways (primary suspension universal in LHB coaches).

Forging Division — ₹16–17 Cr in Q2

Utilization improving; 6-ton hammer now contributing.

Expected to reach ₹75–80 crore for FY26 and ₹100–115 crore for FY27.

Orders coming in from railways. — will materially boost margins as utilziation improves.

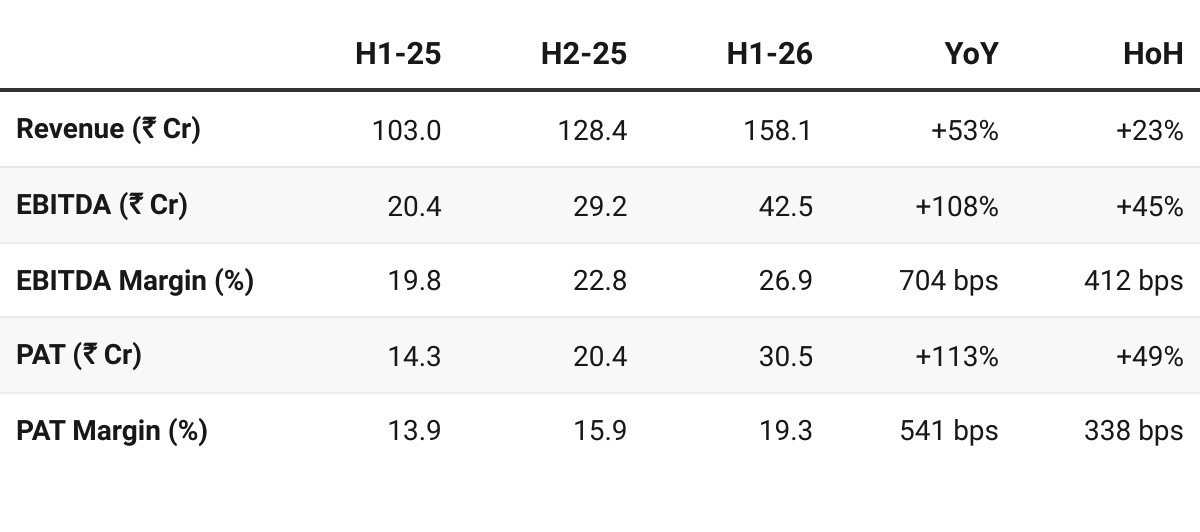

5. H1-26: PAT up 113% & Revenue up 53% YoY

PAT up 7% & Revenue up 10% QoQ

New Products: Exploring defence and road/mining equipment applications; one defence product is already under development.

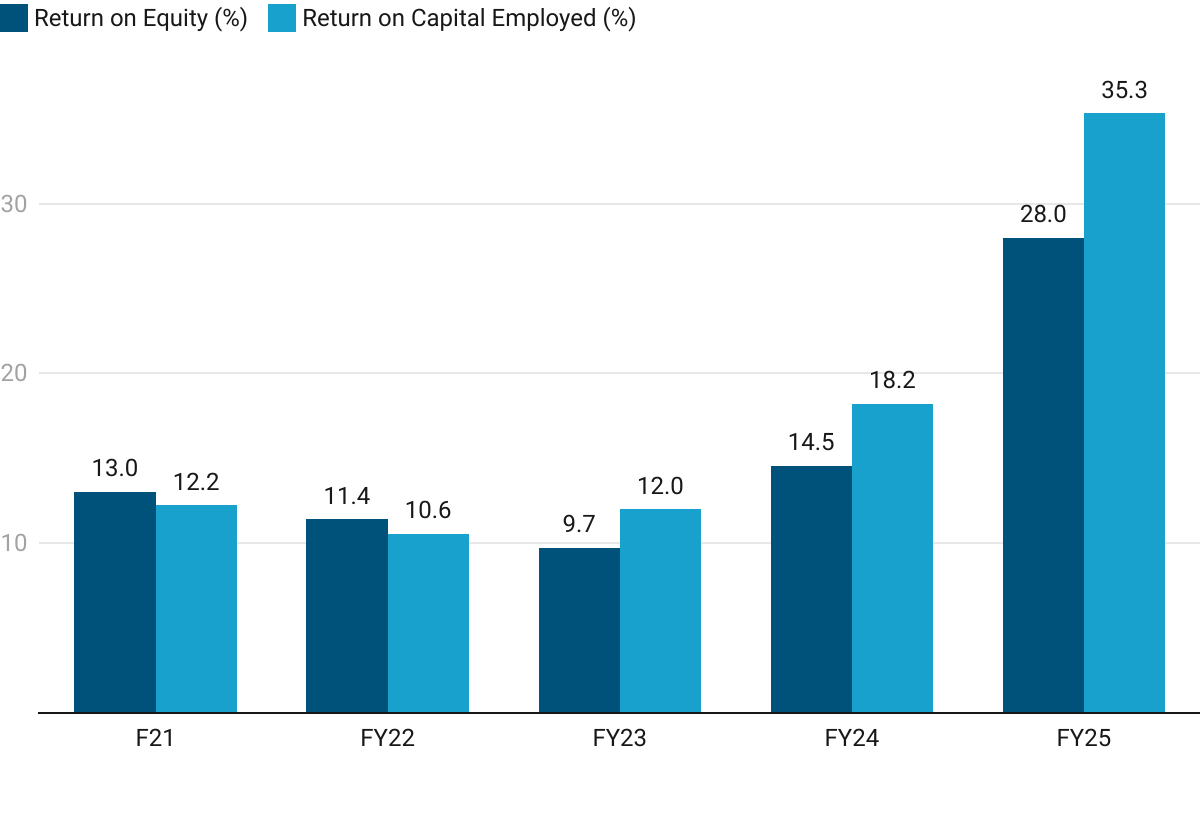

6. Business Metrics: Strong Return Ratios

6. Outlook: 35%+ Revenue CAGR for FY25-27

6.1 FY26 Guidance — Frontier Springs

Order-book provides visibility to FY26 target of ₹375 Cr

Revenue: We focus on achieving a gross revenue amounting to INR 375 crores for the full Fiscal Year ‘25-’26 and further progressing to INR 500 crores gross revenue in the following year.

Possibility of beating guidance: We may cross INR 375 crores, but I’m little conservative. We can cross INR 375 and we can touch INR 400 crores also,

H1 FY26 Margins to be maintained: we hope to close year by this almost the same range of margins.

FY27 Margins: As far as margins are concerned, we will try to have that much of margin, but maybe 1%-2% minus, plus may happen because of the tender business, but we will try to remain in the same margin level for the next year also.

Failure Indication & Brake Application System (FIBA)

Major Future Driver

Samples ready by December 2025 — RDSO approval expected soon.

Trial period ~6–8 months — Commercialisation: H2 FY27

Market size: ₹100 Cr — Frontier share: ₹40–50 Cr per year.

6.2 H1 FY26 Performance vs FY26 Guidance

Revenue: On-track to deliver FY26 guidance.

We are already having INR 187 crores, and we have guidance of around INR 375 crores gross this year. So, we are right on target.

Order visibility:

Order-book in place to support FY26 guidance.

Order-book of ₹200-250 Cr expected by FY26 to end to support FY27 guidance.

As I have committed that INR 375 crores this year, we already have that much of order to close the year, what I have promised.

And for the next year, tenders are already there, and we have already started receiving orders. Around INR 60 crores to INR 80 crores orders have already been received by us. And by the year end, I think we’ll be around INR 200 crores to INR 250 crores order in hand after closing this year.

Margins ahead of plan: H1 EBITDA margin of 27.1% is well above guidance Q1 guidance of 21-22%. H1 margins to be sustained for FY26

FY26 Targets → Achievable if order execution remains on-track

7. Valuation Analysis – Frontier Springs

7.1 Valuation Snapshot — Frontier Springs

CMP ₹3720; Mcap ₹1,465.13 Cr

Margins at the same level as H1 FY26.

Frontier Springs has seen a deep correction compared to levels seen during Q1 FY26 results analysis which has led to value emerging at lower levels

Frontier Springs at 23.5× FY26 P/E is reasonable and at 17.6× FY27 P/E is cheap

Frontier Springs generated ₹11.93 Cr free-cash flow in H1 FY26 and is available at a free-cash flow yield of 0.8% (not annualized) — highlighting the ability of the company to generate free cash-flow

Frontier Spring offers strong earnings growth but limited scope for re-rating from a FY26 perspective.

The opportunity emerges from FY27 and beyond as long as the momentum is maintained

7.2 Opportunity at Current Valuation

Margin Outperformance: H1 FY26 EBITDA margin of 27% is already above the guided 21–23% range during the Q1 FY26 call.

Strong Demand: Outlook for next 5-10 years is strong

Don’t see that demand is going down for next 5-10 years, and it will keep on increasing every year. So, almost 6,000 to 7,000 coaches are being manufactured. So, they require at least next 15,000 coaches to replace ICF coaches. And then again, they need more coaches. So, the demand is going to be there for next 10 years or so. So, there is no problem in that. Demand, is no problem.

At current valuations, the opportunity for fresh entry appears limited. Frontier Springs is better suited for existing investors, who can continue to ride the ongoing momentum and reassess around FY26-end, when visibility into FY27 and FY28 could emerge.

7.3 Risk at Current Valuation

Valuations Already Reflect FY26: At ~35× FY26E and ~26× FY27E P/E, the stock is discounting management’s guidance upfront, leaving limited room for re-rating unless earnings exceed estimates.

Reliance on Indian Railways: Management confirmed Railways will remain the primary customer for the next 5 years. High customer concentration is an inherent risk.

Limited immediate traction in non-railway segments: Management acknowledged limited margin and demand visibility in:

Automotive air springs

Bus/truck applications

This constrains diversification.

Product Range not broad enough to take Frontier to 1,000 Cr revenue

Execution around introduction of new products and acceptance by market needs to be watched for growth beyond FY27

Going to INR 500 crores to INR 1,000 crores, we will definitely require a big jump. So, we have to increase our product line to go up to that level. But going to INR 1,000 crores, bigger jump, we need more product into our kitty.

Revenue depends on wagon builders’ issues (e.g., wheelset shortages): Management noted:

Wheelset shortage had recently disrupted wagon production

Issue is “resolved” now, but such supply-chain issues could reappear

Previous coverage of Frontier Springs

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer