Frontier Springs: PAT growth of 276% & Revenue growth of 99% in Q1-25 at a PE of 43

FY25 revenue growth of 67%. Revenue growth of 40% in FY26 & 40%+ in FY27. Revenue CAGR of 49% for FY24-27. EBITDA margin of 16% sustained in FY25. Strong railway industry tailwinds

The company primarily produces Hot Coiled Compression Springs and forging items, catering especially to the needs of Wagon, Locomotives, and Carriage sectors. Registered with RDSO since 1990, Frontier Springs is a trusted supplier to the Indian Railways

Indian Railways – Our Primary Customer

2. Recovery in PAT in FY24 after a weak FY20-23

3. Strong FY24: PAT up 79% and Revenue up 26% YoY

4. Strong Q1-25: PAT up 276% and Revenue up 99% YoY

PAT up 38% and Revenue up 15% QoQ

5. Return ratios: Strong improvement in FY24

6. Strong Outlook: Revenue growth of 67% in FY25

i. FY25: Revenue growth of 67%

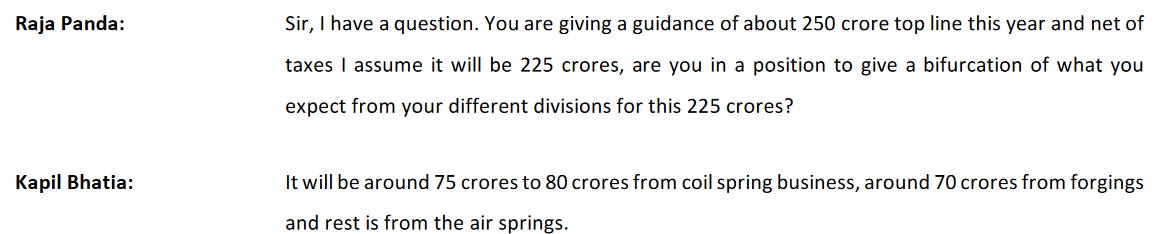

FY24 Revenue of about Rs 135 cr to grow to Rs 225 cr in FY25 i.e. 67% growth

Our revenue for the quarter aligns with our previously stated guidance, targeting a gross top line of ₹240-250 crores for FY25.

ii. FY26: 40% revenue growth

With Rs 250 cr revenue for FY25 (including GST) growing to Rs 350 cr implies a growth of 40%

this year we are targeting 250 next year will be around 350.

ii. FY27: 40%+ revenue growth

With Rs 350 cr planned revenue for FY26 (including GST) growing to Rs 500 cr implies a growth of 40%+

in last concall I have already told that by 26-27 we will be targeting 500 crores business which is gross

iv. Order book 3.4X FY25 expected revenue

With Rs 250 cr revenue for FY25 (including GST) the order book of Rs 850 crore is 3.4X FY25 expected revenue.

As far as orders are concerned, we have a good order book almost Rs.850 crore orders are in hand includes forging, air springs and coil springs

7. PAT growth of 276% and Revenue up 99% in Q1-25 at a PE of 43

8. So Wait and Watch

If I hold the stock then one may continue holding on to Frontier Springs

While the past track record of Frontier Springs is not exceptional, one expect a strong future given the underlying orders in place to support the business growth.

Our coil springs segment has seen substantial demand, and we have secured significant orders that set a strong foundation for FY25.

The air springs segment has also performed well, with a notable order from the Indian Railways. This order is progressing on schedule, and we anticipate continued strong demand in the coming quarters.

Furthermore, we are on track with the installation of our 6-ton hammer, which is expected to begin commercial production by mid-Q2FY25. This new capacity will enable us to produce higher tonnage forgings and cater to new industries, enhancing our product offerings and margins. We expect this investment to start contributing to our performance from Q3FY25.

Outlook is strong for FY-25

In first two quarters we will be doing it like this around 120 to 140 crores

The demand for our products remains robust, and we have a strong order book with excellent visibility of future demand. We remain confident in achieving our stated guidance and look forward to a future full of growth and prosperity

Outlook is very positive given guidance of revenue CAGR of 49% for FY24-27

New product (Air Springs) to significantly contribute to the topline growth

New (Air Springs) to help improve the margin profile of the business

Strong Industry Tailwinds and growth visibility

The bottom-line growth can be expected to be in line with the top-line growth given the 19.21% Q1-25 EBITDA margin gives it a cushion for FY24 margins to be sustained into FY25.

9. Join the ride

If I am looking to enter Frontier Springs then

Frontier Springs has delivered PAT growth of 276% and revenue growth of 99% in Q1-25 at a PE of 43 which makes the valuations fully priced.

Outlook for 67% revenue growth in FY25 with bottom-line growing in line with top-line growth the top-line on account of EBITDA margin expansion at a PE of 43 makes the valuations fair from a FY25.

Outlook for 49% revenue CAGR for FY24-27 with bottom-line growing in line with top-line growth the top-line on account of EBITDA margin expansion at a PE of 43 creates opportunity in Frontier Springs over the longer term.

The performance for FY24 looks well discounted in the price. The opportunity in stock is from the performance from FY25 onwards.

A PE of 43 looks rich in the short term hence positions need to be built over time over bad days when the stock is not doing well. Reaction in stock price will be seen if execution for even one quarter is not in line with the guidance given.

The risk of investing in a small company with less than Rs 115 cr of revenue needs to be kept in mind.

Nice one, the growth and numbers are mind boggling.

Interested to see the guidance in action and waking the talk.