Elecon Engineering Company: PAT growth of 49% & revenue growth of 24% for 9M-24 at a PE of 34

ELECON has delivered sequential QoQ PAT growth in the last 4 consecutive quarters. ELECON is guiding for 31% revenue growth and 42% EBITDA growth. EBITDA margin expansion to 24% from 22% in FY24

1. Manufacturing of Industrial Gear & Material Handling Equipment (MHE)

elecon.com | NSE: ELECON

One of the largest manufacturers of industrial gears in Asia

India’s largest Industrial gear solution provider

~34% share in Organized Market in India

Revenue Split

2. FY20-23: PAT CAGR of 38% & Revenue CAGR of 12%

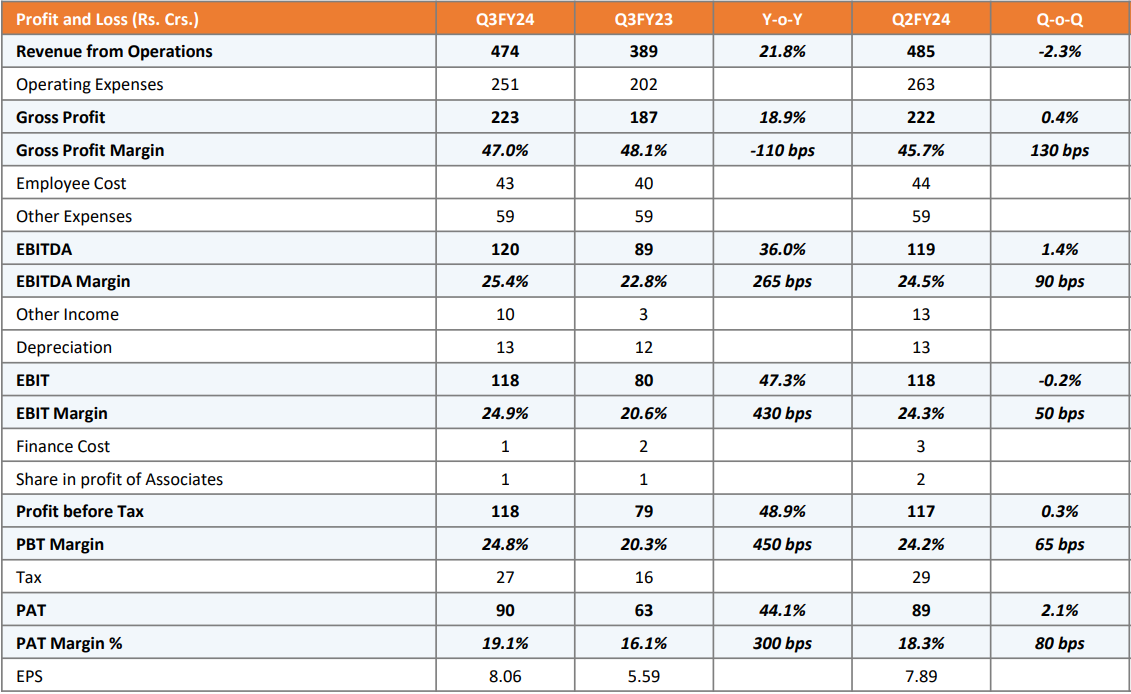

3. FY23: PAT up 69% & Revenue up 26%

4. Strong H1-24: PAT up 36% & Revenue up 23% YoY

5. Strong Q3-24: PAT up 44% & Revenue up 22% YoY

PAT up 2% & Revenue down 2% QoQ

6. Strong 9M-24: PAT up 49% & Revenue up 24% YoY

7. Business metrics: Strong and improving return ratios

8. Strong outlook: 31% revenue growth in FY24

i. FY24: 31% revenue growth

9M-24 revenue is Rs 1373 cr. To achieve the Rs 2000 cr revenue guidance for FY24, the asking rate for Q4-24 is Rs 627 cr of revenue. This would be a 48% YoY growth over Q4-23 and 32% QoQ growth over Q3-24. 32% QoQ growth looks like a stiff challenge but the management seems confident of achieving it and have confirmed it in their Q3-24 earnings call.

Moving to the financial aspects, we had mentioned our revenue guidance of INR 2,000 crores for FY '24 which we are expected to reach in spite of challenges due to current geopolitical scenario as well as softening of the steel-based raw material prices.

ii. FY24: EBITDA growth of 41%

EBITDA margin expansion to 24%+ in FY24 from 22% in FY23 would mean that EBITDA would grow from Rs 339 cr in FY23 to Rs 480 cr in FY24 i.e. 41% growth.

We expect our EBITDA margins and in absolute terms will remain 24% plus.

iii. Orders in place to support revenue guidance

last order which we received in January, which is of INR83 crores, is not included in our order book, open order book portion of INR791 crores as of 31st December 2023. If we include that, my total order book portion will be INR874 crores.

our deliveries are extremely fast. So, the time that we take to process and execute is very fast. So, you see a big consumption that takes place.

9. PAT growth of 49% & Revenue growth of 24% in 9M-24 at a PE of 34

10. So Wait and Watch

If I hold the stock then one may continue holding on to ELECON

Based on 9M-24 performance, ELECON looks on track to deliver the strongest revenue & PAT in FY24

ELECON is in the middle of a strong run and has delivered sequential QoQ growth in PAT in the last four consecutive quarters starting from Q4-23

One can look forward to a strong Q4-24 given the confidence of the ELECON management to deliver Rs 2,000 cr of revenue in FY24 and then assess the FY25 guidance.

We shall provide FY '25 revenue and EBITDA margin guidance in Q4 FY '24 earnings call

11. Join the ride

If I am looking to enter ELECON then

ELECON has delivered PAT growth of 49% and revenue growth of 24% in 9M-24 at a PE of 34 which makes the valuations fairly valued in the short term.

With a FY24 revenue growth outlook of 31% and EBITDA growth of 41% at a PE of 34 makes the valuations fairly valued in the short term.

One can expect a strong Q4-24 as ELECON works to deliver its guidance of Rs 2,000 cr and then assess the FY25 guidance.

One may not see opportunities in ELECON in the short-term at a PE of 34. Additionally one can see a reaction in case of a weak quarter given that the PE is 30+

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer