Dynacons Systems & Solutions: 65-85% revenue growth in FY24 at a PE of 20

Growth to pick up pace in FY24 given that PAT was up 209% & revenue up 85% yoy in Q1-24 after consistently growing at revenue CAGR of 31% & PAT CAGR of 74%, yoy, every year for the last 7 years

1. An IT infrastructure services company

dynacons.com | NSE : DSSL

Dynacons Systems & Solutions Ltd. (DSSL) is an IT company with its headquarters at Mumbai and branches all over India. Established in 1995, Dynacons undertakes all activities related to IT infrastructure including infrastructure design and consulting services, turnkey systems integration of large Network and Data Centre infrastructures including supply of associated equipment and software, onsite and remote facilities management of multi location infrastructure of domestic clients.

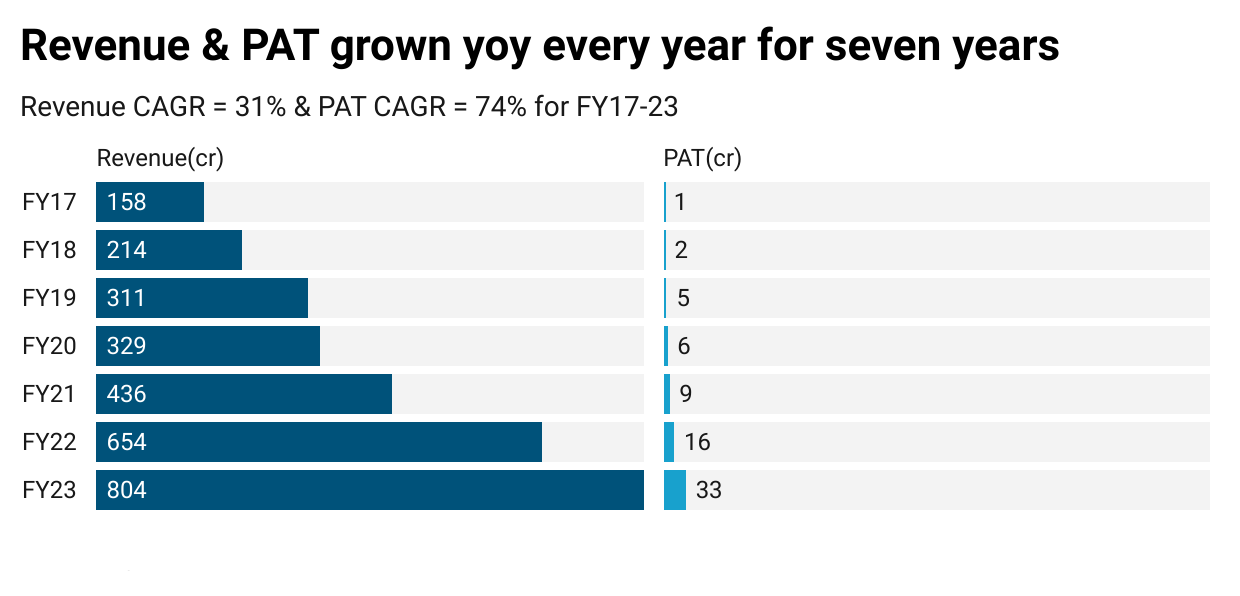

2. FY17-23: Track record of consistent growth

3. FY23: PAT up 104% and Revenue up 23% YoY

Revenue from operations for FY 2023 at Rs 80,677 lakhs was higher by 23% over the previous year. The profit after tax stood at Rs 3,345 Lakhs for the current year, an increase of 104% over the previous year

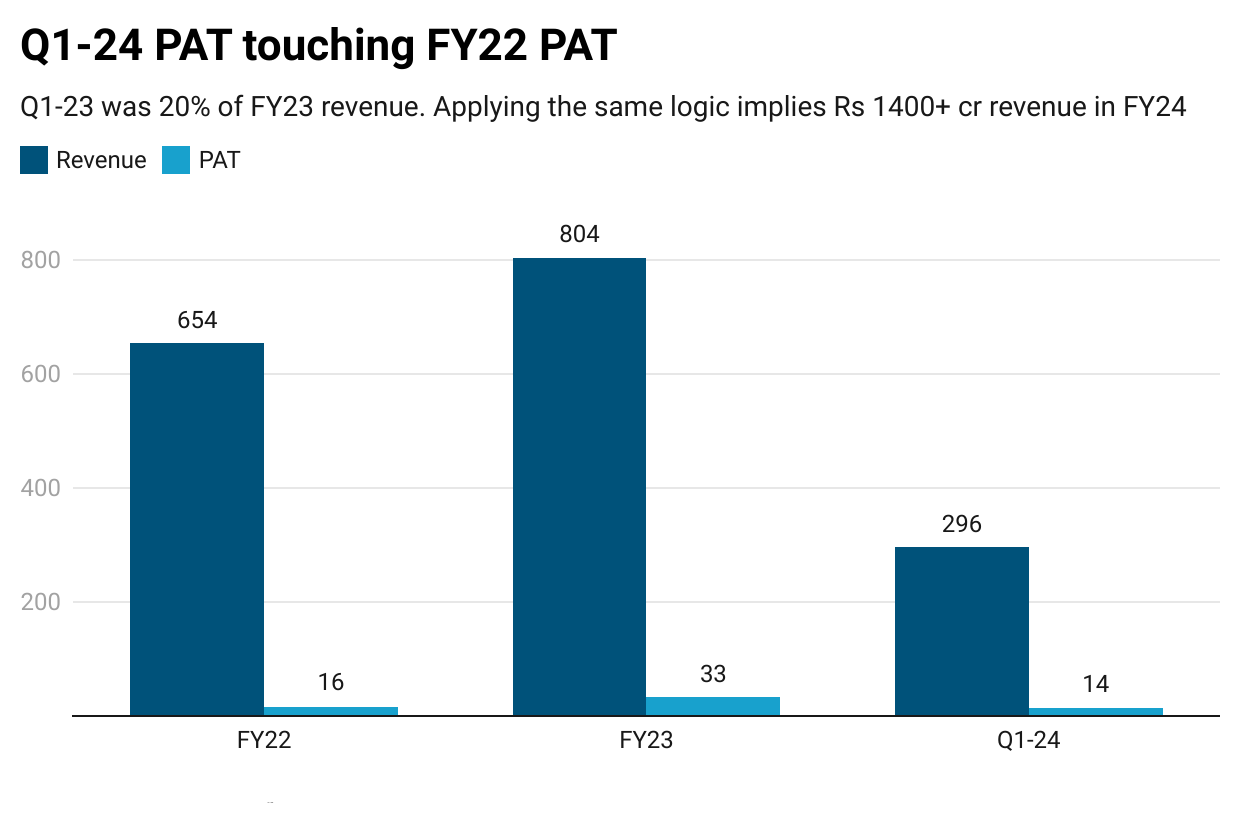

4. Q1-24: PAT up 209% and Revenue up 85% YoY

5. Business metrics are strong and consistent

The business has delivered returns consistently. Cash conversion has been weak

6. Outlook: 65-85% revenue growth in FY24

In the absence of any management commentary or public information on the DSSL, one is relying on past trends repeating themselves in FY24. Q1-24 has contributed to 20-22% of annual revenue in FY22 and FY23. Overall overage for the five years is 21% of annual revenue coming from Q1.

Based on a 20-22% range FY24 revenue is estimated to be Rs 1322-1489 cr which translates to a 65-85% growth over FY23.

7. 65-85% revenue growth in FY24 at a PE of 20

8. So Wait and Watch

If I hold the stock then one may continue holding on to DSSL. This efficiently managed business consistently generates growth consistently over the long term.

There can be a case for PE expansion in FY24 as it crosses Rs 1,000 cr revenue and may get noticed by those who may be filtering it out based on size.

One needs keep watching it quarter over quarter as the trend for consistent year on year top-line and bottom-line growth continues

All the views on DSSL are based on published financials only. In the absence of management commentary, one can that call that there is significant headroom to grow for it continues on a 30% long term top-line growth trajectory.

9. Or, join the ride

If I am looking to enter the stock then

DSSL has achieved an impressive a strong Q1-24 on the back of an excellent FY23 where it doubled its PAT. The outlook continues to be strong with the expectation of a 65-85% top-line growth. Keeping the past performance along with the outlook for FY24, the PE of 20 looks quite reasonable.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades