Dr Lal PathLabs - Growth is the challenge

A high quality company irrespective of the growth challenges.

Company Overview

Dr Lal PathLabs Limited is an Indian service provider of diagnostic and related healthcare tests. Based in New Delhi, the company offers tests on blood, urine and other human body viscera.

Share Details

NSE:LALPATHLAB

Closing Price = 2020 (2-Jun-23)

52 Week High = 2750 (27% above closing price)

52 Week Low = 1762.05 (15% below closing price)

P/E = 70

Market Cap = 16,762.15 cr ( ~$ 2 bn)

Quality: Returns on capital employed in cash

LALPATHLAB has delivered high quality company results consistently over the last 9 years.

A PAT ranging between 15-18% is a reflection of the state of the industry where pricing power is limited.

The high ROE, ROCE and cash conversion indicates that the management has run the company efficiently

You cannot fault someone who has bought NSE:LALPATHLAB based on the quality of the company

Growth

When we start looking at growth then the consistency in growth is sold, even if we ignore one bad year i.e. FY22-23 where growth negative.

The issue in growth is that we look at a stock to make money. We are looking for a multi-bagger. Any stock growing at compounded growth rate rate of 15% while never add explosiveness in your portfolio. At best it can add consistency and solidity to your portfolio.

On top of it the management has given a forecast of 8-9% volume growth for FY23-24. This kind of tepid growth outlook does not make it a high growth stock.

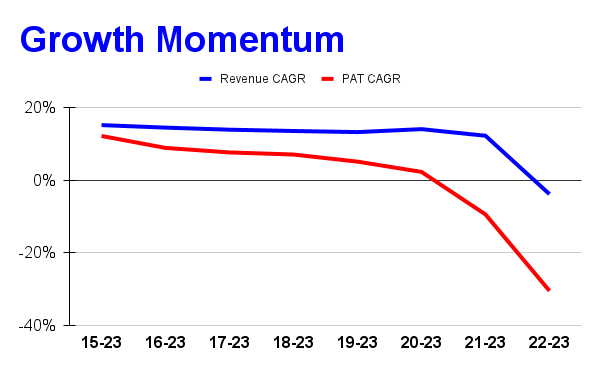

There is another problem with the growth numbers, it is quite clear that the growth momentum is stalling as shown in the graph below

The way to interpret the graph is as follows, for revenue the compounded annual growth rate (CAGR) for FY15-23 was 15%,. The revenue CAGR for FY21-23 was 12% and -4% for FY22-23. The slowing of revenue growth is visible clearly from this graph.

When we look at PAT growth the slowing of PAT is visible more clearly. PAT CAGR growth for FY15-23 at 12% slowed to 2% PAT CAGR growth for FY20-23, crashed to -30% for FY22-23

The growth momentum outlook is not very encouraging given the 8-9% volume growth indicated by the management for FY23-24

So What????

If I own the stock, I may keep it based on my historic returns, future return expectations, and availability of alternative stock ideas

If I don’t own the stock, now may not be the best time to enter. I don’t want to buy a stock which is at PE of 70 and the growth momentum has crashed. Better to see wait and see the what the management can do to get the growth momentum on track.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades