CMS Info Systems: PAT growth of 19% & Revenue growth of 14% in H1-24 at PE of 19

CMSINFO is on track to meet its revenue guidance of guidance Rs 2500-2700 cr by FY25 while consistently improving its margin.

1. Largest Cash Management company in India

cms.com | NSE : CMSINFO

ATM Cash Management #1 Player

Retail Cash Management (RCM) #1 Player

Cash-in-Transit (CIT) #1 Player

2. FY19-23: Track record of growth with expanding margins

3. Strong FY23: PAT up 33% and Revenue up 20% YoY

4. Strong Q1-24: PAT up 22% and Revenue up 13% YoY

PAT up 6% & Revenue up 2% QoQ

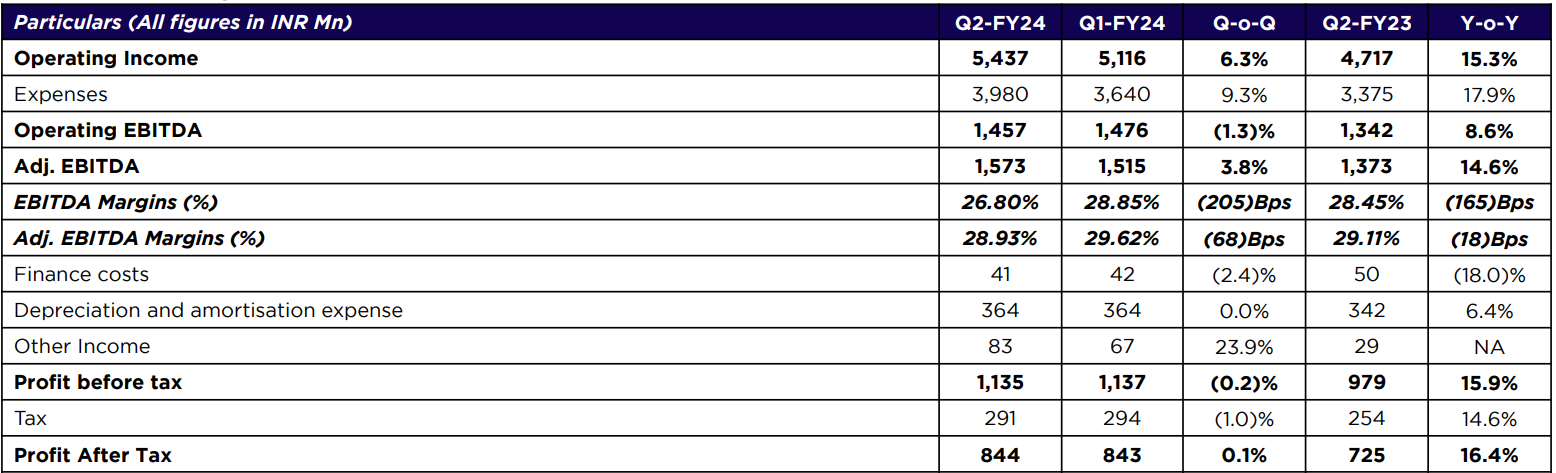

5. Strong Q2-24: PAT up 16% & Revenue up 15% YoY

PAT up 0.1% & Revenue up 6% QoQ

6. Strong H1-24: PAT up 19% & Revenue up 14% YoY

7. Business metrics: Solid return ratios converting PAT to cash

8. Outlook: 14-19% revenue CAGR for FY23-25

Moving from Rs 1915 cr revenue in FY23, to Rs 2500-2700 cr by FY25 implies a revenue CAGR of 14-19% for FY23-25.

Based on our current momentum at half of this year, we feel confident of achieving our FY ’25 revenue target of doubling our revenue on a FY ‘21 basis from INR1,300 crores to a range of INR2,500 crores to INR2,700 crores.

Margins, we have not guided towards at all. We have no margin guidance at all, and we will refrain from giving any margin guidance.

9. PAT growth of 19% & Revenue growth of 14% in H1-24 at a PE of 19

10. So Wait and Watch

If I hold the stock then one may continue holding on to CMSINFO

Based on H1-24 performance, CMSINFO looks on track to deliver a strong yearly performance in FY24

On an annual run rate CMSINFO is on track to deliver as per the revenue guidance set out by the management.

CMSINFO is in the middle of a strong run. One can ride along with the strong quarterly performances.

Q2’FY24 is our sixth consecutive quarter with 20%+ YoY earnings growth.

While a 14-19% revenue CAGR for FY23-25 may not sound exciting, the consistent improvement in PAT margins has ensured that bottom-line is growing faster than the top-line

11. Or, join the ride

If I am looking to enter CMSINFO then

CMSINFO has delivered PAT growth of 19% & Revenue growth of 14% in H1-24 at a PE of 19 which makes valuations acceptable.

Outlook for top-line growth at a CAGR of 14-19% for FY23-25 with expectation of bottom-line growing faster than the top-line makes the valuations acceptable.

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades