Capacit’e Infraprojects Q1 FY26 Results: Weak Quarter, Confident of Achieving FY26 Guidance

Guidance of 20% CAGR for FY25-28. Despite a weak Q1 a strong order book and attractive valuations create a compelling case for upside as execution accelerates

1. Construction Company

capacite.in | NSE : CAPACITE

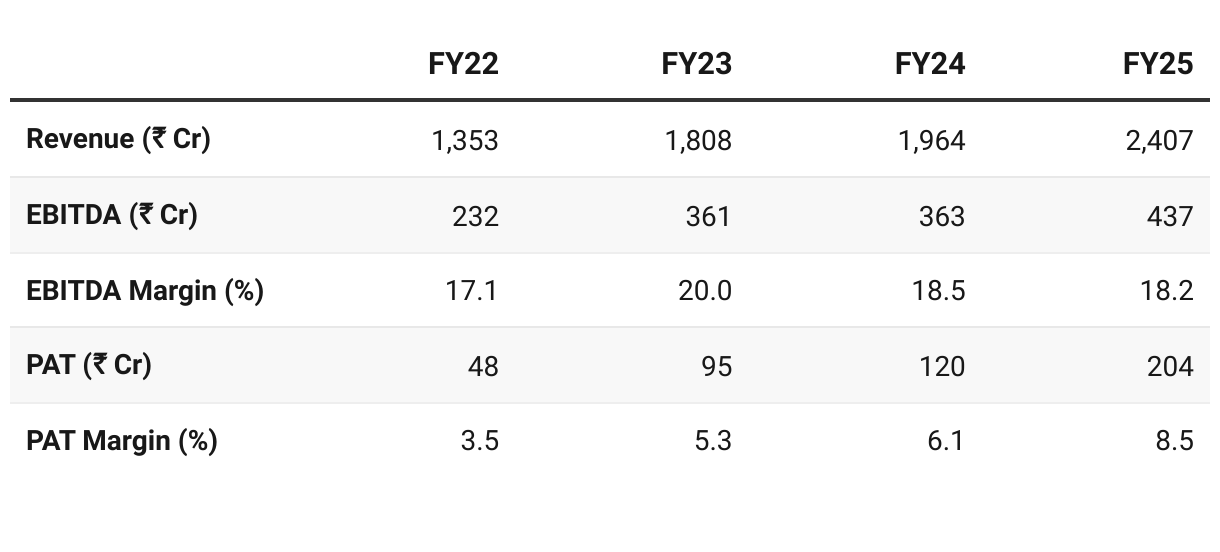

2. FY22-25: PAT CAGR of 62% & Revenue CAGR of 21%

2.1 What Changed Between FY22–25

Shift to High-Margin Public EPC: Benefits: price escalation, assured funding, smoother billing

Execution Focus & Cost Leverage: Fewer, larger projects from FY23.

Higher per-site revenue, flat employee cost, stable EBITDA margin

Working Capital Efficiency: NWC cycle reduced by ~37 days.

Driven by: faster billing (MHADA/CIDCO), BG-backed retention release, better private client selection.

Pure Building Focus: No roads/rail — only residential, healthcare, & commercial

Outcome: entry barriers, client stickiness (Lodha, MHADA), and higher margins vs infra peers.

3. FY25: PAT up 70% & Revenue up 22% YoY

Revenue growth driven by robust execution and new order inflows.

EBITDA margin dipped due to:

Conservative accounting

Higher depreciation from capex in site establishments

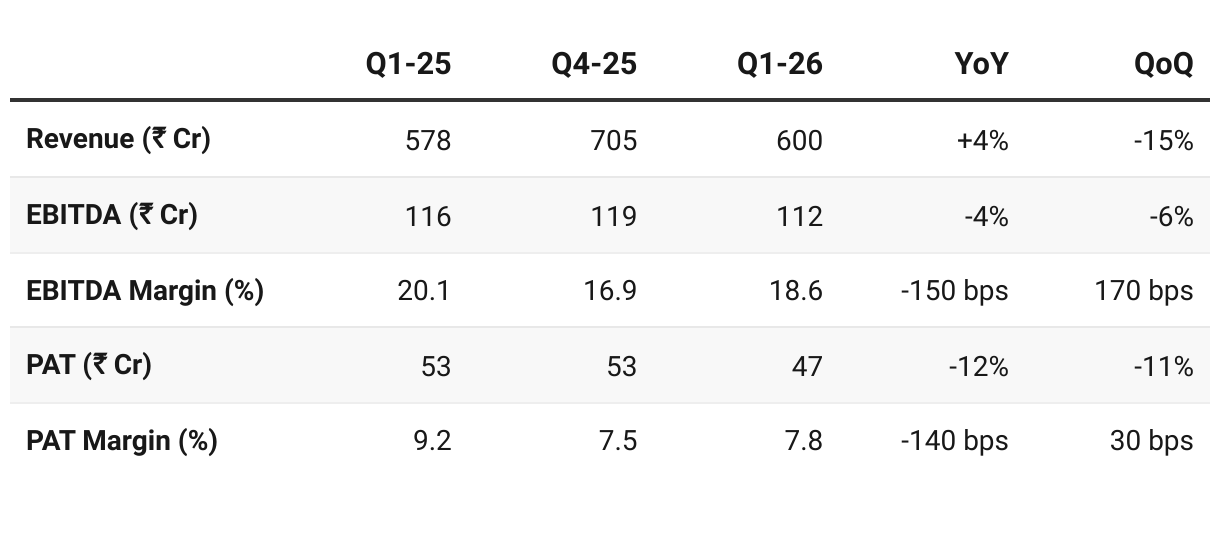

4. Weak Q1-26: PAT down 12% & Revenue up 4% YoY

Revenue loss of ~₹75 Cr due to early monsoon & temporary labor migration.

Execution to accelerate from Q2/Q3 – monsoon & Eid impact is temporary; large projects (CIDCO, MHADA, NBCC, Signature Global) will drive growth.

Management confident of sustaining margins at upper end of 16.5–17.5% for FY26, despite cost pressures

Q1-26 EBITDA margin at 18.6% is above guidance;

Q1 FY26 was soft on revenue growth due to external factors, but underlying execution efficiency and margin performance remain strong. With a robust order book and improving collections, the company looks on track to deliver its FY26 guidance, with stronger performance expected in H2.

5. Business Metrics: Weak — Improving Return Ratios

Return Ratios following the trend of margin expansion

6. Outlook: 20% revenue CAGR for FY25-28

Confident of 20% growth and margins at upper end of guidance band

6.1 Guidance & Outlook for FY26 and Beyond

FY26 Guidance — Capacit’e Infraprojects

Revenue Growth: Targeting 20% YoY growth,

EBITDA Margin: Maintain in the range of 16.5–17.5%

Order Inflow: So we have already given a target for the current full year, which is about INR4,000 crores to INR4,500 crores.

Vision 2028 – Capacit’e Infraprojects

Target ₹4,000+ Cr revenue by FY28 with 20%+ CAGR driven by EPC project execution.

Maintain 16.5%–17.5% EBITDA margins, including other income, through operational efficiency.

6.2 Q1 FY26 Performance vs FY26 Guidance

Revenue:

Q1 revenue at was below run-rate for ~₹2,900 Cr FY26E.

Guidance maintained — strong catch-up expected from Q2, with sharp acceleration in H2 FY26 .

EBITDA & Margins:

EBITDA margin 18.6%, above guidance band (16.5–17.5%).

Management confident of sustaining upper end of guidance for full-year.

PAT:

PAT slightly below FY26E run-rate.

Deferred profit recognition from NBCC and Signature Global to start flowing from Q2 onwards, supporting growth.

Cash Flow & Debt:

Collections at ₹543 Cr vs revenue of ₹599 Cr — healthy 91% realization in Q1.

Management reiterated positive cash flow generation for FY26 with ₹65 Cr asset monetization planned.

Q1 FY26 was soft on topline but strong on margins and collections.

Revenue miss is seasonal/temporary; execution to normalize from Q2 and accelerate in H2.

Margins, debt, and collections are trending better than guidance, lending comfort.

7.2 Opportunity at Current Valuation

Strong Growth Visibility: ₹11,254 Cr order book (~4.8× FY25 revenue) ensures 3+ years of revenue visibility, with CIDCO, MHADA, NBCC, and Signature Global projects driving execution momentum from H2 FY26.

Margin Comfort: Management expects to sustain margins at the upper end, supported by selective bidding and operational efficiency.

Improving Cash Flows: Collections at 91% of Q1 revenue show discipline in working capital management. Management expects FY26 to be cash flow positive, a structural improvement vs earlier years.

Valuation Comfort: Trading at ~11× FY26E P/E and 5.8× EV/EBITDA, valuations are reasonable for a 20% CAGR story. By FY28, multiples compress further to ~8× P/E and 4.2× EV/EBITDA, opening room for re-rating.

Catalysts: Execution pickup in H2, order inflows above guidance (₹4,000–4,500 Cr target), debt reduction, and consistent delivery can drive investor confidence and valuations higher.

Opportunity Rating: High — Strong order book + attractive valuations create a compelling case for upside as execution accelerates. However, one most be ready to go through a phase of weakness in the stock till the promised momentum is seen in H2 FY26

7.3 Risk at Current Valuation

Execution Risk: Heavy reliance on large public projects (CIDCO, MHADA, NBCC). Any delay in approvals, site readiness, or execution pace can derail the 20% growth guidance.

Seasonality & External Factors: Monsoon, elections, and regulatory stoppages (e.g., NGT in NCR winters) could cause quarterly volatility in revenue recognition.

Labor Shortages: Structural shortage of skilled manpower due to overseas demand; despite tech-enabled tracking, availability could remain a growth bottleneck.

Working Capital Intensity: Government/EPC projects are back-ended on cash flows. Elevated contract assets could strain operating cash flows if collections falter.

Profit Recognition Lags: Deferred recognition from NBCC, Signature Global, and JVs may create earnings lumpiness and mismatch between execution and reported profits.

Margin Sensitivity: Input cost inflation (steel, cement) or unfavorable contract terms could squeeze EBITDA margins below guidance.

Risk Rating: Medium — Structural strengths are intact, but execution, labor remain key watchpoints that could cap near-term rerating.

Previous Coverage of CAPACITE

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

Adding to the risk is extended monsoons. Besides long working capital days which they are trying to improve. And their conversion to cash of EBITDA is also needs to be watched for. Your input ?