Bharat Wire Ropes: PAT growth of 61% & Revenue growth of 11% in 9M-24 at a PE of 23

BHARATWIRE guiding 30%+ volume growth via improvement in capacity utilization over 18-24 months. Margin expansion to drive PAT growth higher than top-line growth. At an attractive free cash flow yield

1. Manufacturer of specialty steel wire, steel wire ropes, slings & strands

bharatwireropes.com | NSE : BHARATWIRE

One of the largest manufacturer of Steel Wire Ropes in India

The wire rope product is generally a replacement market, it is almost 60% and our products are being exported through almost 50-55 countries

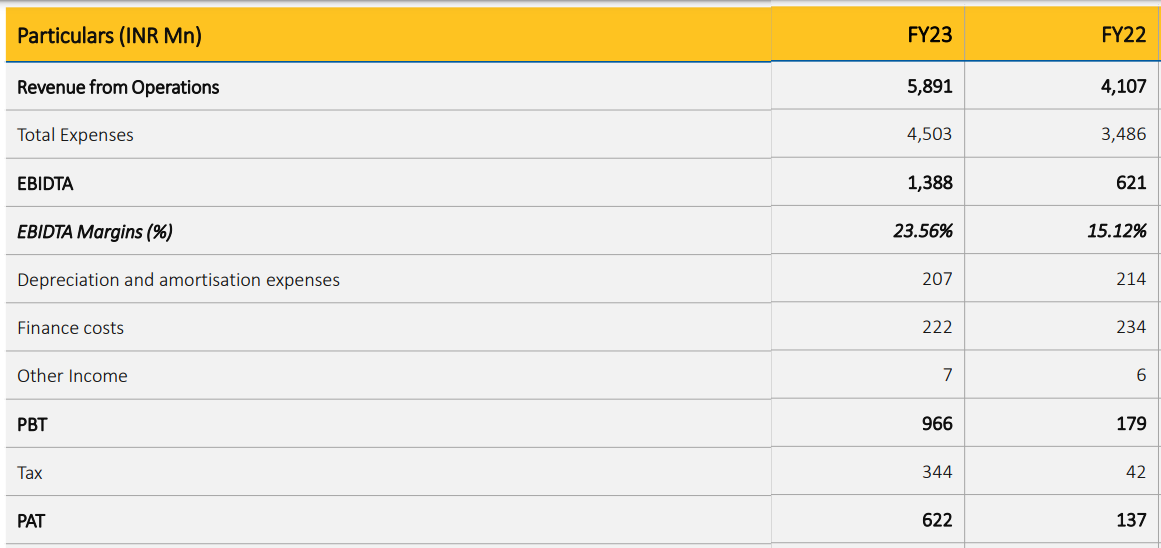

2. FY21-23: Recovery started from FY22 after losses in FY21

3. Strong FY23: PAT up 354% & Revenue up 43% YoY

4. Strong H1-24: PAT up 76% & Revenue up 12% YoY

5. Strong Q3-24: PAT up 39% & Revenue up 9% YoY

PAT up 8% and Revenue down 1% QoQ

6. Strong 9M-24: PAT 61% & Revenue up 11% YoY

7. Business metrics: Improving return ratios

Margin expansion in FY23 reflected in improvement of return ratios

8. Outlook: Volume growth of 33-40% by FY26

i. Volume growth of 33-40% by FY26

Capacity utilization increase from 60% to 80-85% implies a volume growth of 33-40%

Q3-24: capacity utilization stands at around 60% for this quarter.

Right now the entire focus of the company is to maximize the utilization which would be 80%, 85%. In the next 18 to 24 months.

I think we were focusing on 10-15% growth, and we are on track.

ii. Order book in place for Q4-24

The order book is approximately two to three months, which would be in the range of INR 150 crores.

9. PAT growth of 61% & Revenue growth of 11% in 9M-24 at a PE of 22

10. So Wait and Watch

If I hold the stock then one may continue holding on to BHARATWIRE

Based on 9M-24 performance, BHARATWIRE looks on track to deliver the strongest yearly performance in terms of revenue and PAT in its history

BHARATWIRE is in the middle of a strong run and has delivered sequential QoQ growth in PAT for 4 consecutive quarters starting Mar-23

If you look at our numbers for last 3 years, every QoQ we have shown consistent growth. So, we expect that H2 should be definitely in the same growth lines compared to the first H1.

BHARATWIRE is delivering margin expansion

Last 4 years, we were operating at 13% EBITDA in 2021, which has improved to 15% in FY22 and further to 24% in FY23. And now, currently we are operating at 27% in FY24 nine months.

11. Or, join the ride

If I am looking to enter BHARATWIRE then

BHARATWIRE has delivered PAT growth of 61% & Revenue growth of 11% in 9M-24 at a PE of 22 which makes valuations quite attractive.

BHARATWIRE delivered Rs 74.8771 cr of free cash flow in H1-24 against a market cap of Rs 2,058 cr. As of H1-24 end it is available on a free cash flow yield of 3.6% (not annualized) which makes the valuations quite attractive.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer