Archean Chemical Industries - 2X in 2-3 years

Potential for high growth & high returns, yet attractively priced

Company Overview

Archean Chemical Industries Limited (ACI) is a more than 10 year old leading specialty chemicals manufacturing company based in India with a wide presence in the global markets.

ACI is the largest exporter of bromine and industrial salt in India. It has an integrated production facility located at Hajipir, Gujarat and has it our own brine reserves in the Great Rann of Kutch in Gujarat.

On the capex, we are in the growth phase and obviously given the growing demand for the three products, we continue to invest in expanding our capacity and capability.

Management comment during earnings call

Share Details

NSE: ACI( archeanchemicals.com)

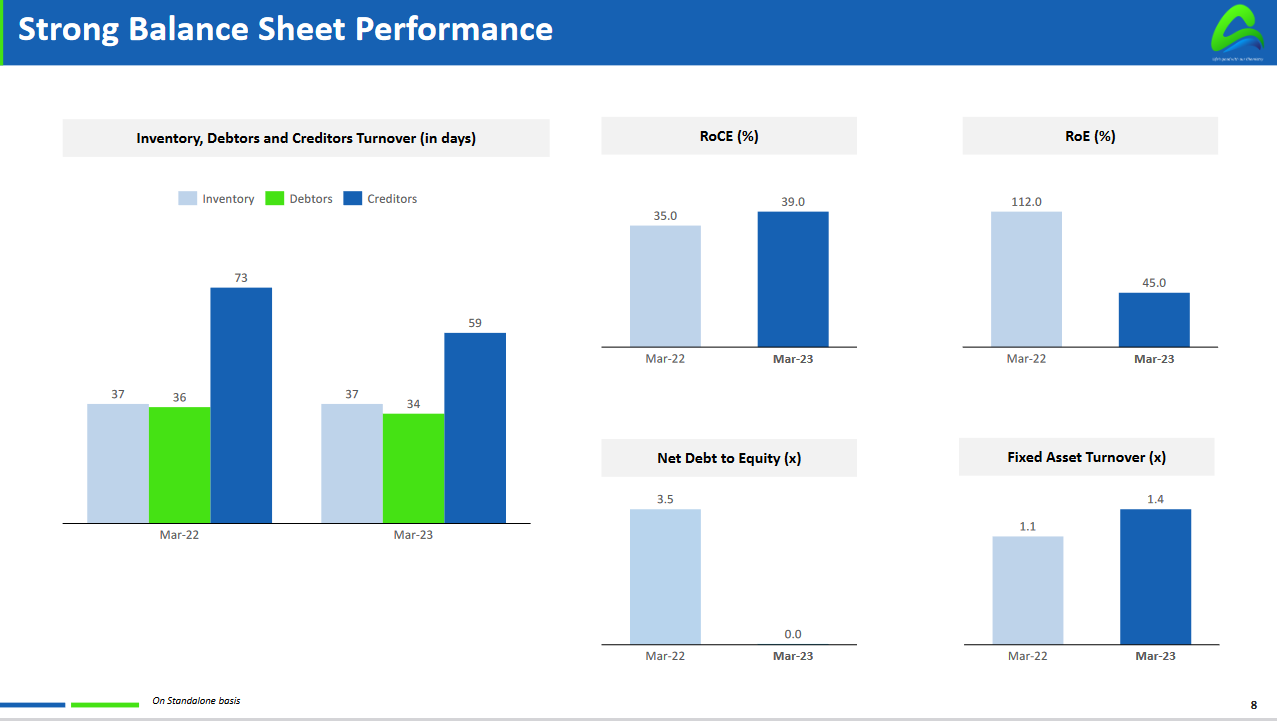

Quality: Returns on capital employed in cash

The company has a significant brownfield and green field expansion coming up and the efficient management of capital in the past gives confidence in the ability to manage the currently planned capex spend efficiently and generate returns from it.

Growth

The past performance of the company to grow both the top line and the bottom line while generating free cash flow gives confidence in the company’s ability to deliver growth in the future.

Outlook

Future growth is expected from

Brownfield expansion - expanded bromine and industrial salt capacities

Greenfield expansion - expand into downstream bromine derivative performance product

From various discussions in the Q3 and Q4-23 earnings call, the management has indicated that greenfield expansions is expected to add Rs 600-700 crores to the top-line i.e an additional 40-50% on the FY23 top-line. Overall, the management is giving an indication that the company will grow by two times.

The growth is not expected to dilute margins as indicated by the management

I think our margin target has always been in the 40%, 45% range give or take.

FY24, growth to be driven by industrial salts

The capacity utilization for salt has been more than 100% for FY23 and is expected to sustain the growth momentum in coming quarters given the order book.

We're the only manufacturers of Sulphate of potash, natural sea brand in India. We are negotiating with a few customers and expect to increase production, which will reflect in next year's business performance

FY25 will see the impact of the brownfield and greenfield expansions

Coming to industrial salt, we will be adding additional capacity on the washing lines and increase by another 250 tons per hour capacity and is expected to come in the latter part of FY24

We will be expanding our product portfolio of bromine performance derivatives like flame retardants, clear brine fluids and bromine catalyst at Jhagadia. This greenfield site and expansion at Jhagadia is on track and expected to commence production by the end of FY24.

So What????

If I currently hold the stock, I may continue holding it based on my past returns, expectations for future returns, and the availability of alternative stock ideas. The intention is to retain it for as long as one can see the commitment of the management to grow the company by two times getting executed on the ground

If I don't currently own the stock, I might consider entering it. One can view ACI as an attractively priced stock at a PE of 17, considering that has the potential to grow by two times without diluting the 40-45% EBIDTA margin. One can see the impact of the expected growth for the full year in FY25 and partially in H2-24.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades