Anant Raj: PAT growth of 82% & revenue growth of 48% for Q1-25 at a PE of 58

Revenue CAGR of 34% for FY24-29 on the back of strong revenue visibility. Rs 15,000 cr revenue over a period of 5 years from real estate. Rs 3300 cr of rental income from data centers by FY29

1. Real Estate Development, Construction & Infrastructure Development

anantrajlimited.com | NSE: ANANTRAJ

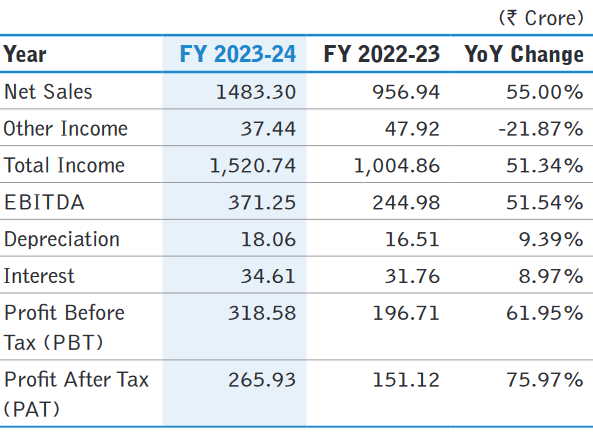

2. FY21-24: PAT CAGR of 189% & Revenue CAGR of 78%

3. Strong FY23: PAT up 175% & Revenue up 107%

4. Strong FY24: PAT up 71% & Revenue up 51%

5. Strong Q1-25: PAT up 82% & Revenue up 48% YoY

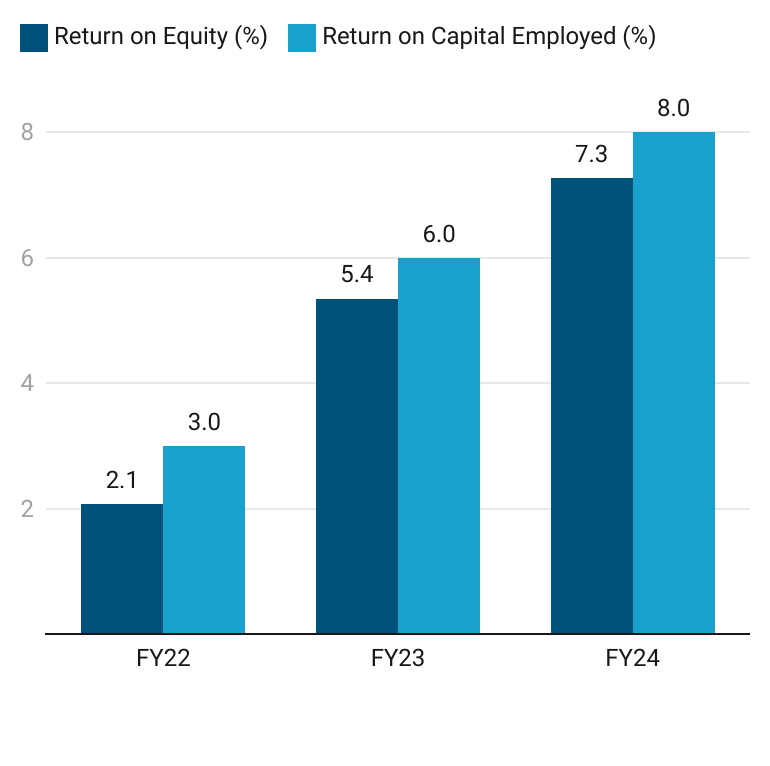

6. Business metrics: Improving but weak return ratios

7. Strong outlook: Revenue growth of 35%+

i. FY24-29: Strong Revenue visibility in real estate business

Potential to grow from Rs 1,500 cr revenue in FY24 to Rs 3000 cr per year by FY29.

~INR 15,000crs of revenue potential in next 4 to 5 years from residential sales in Sector 63A, Gurugram

ii. FY24-29: Strong Revenue visibility in Data Center Business

One can expect rental of Rs 3300 cr by FY29.

Scale up to 307 MW IT Load Data Center within the next 4 to 5 years

Converting existing 5.66 msf commercial property into a 157 MW Data Centre, with another 150 MW expansion planned in Rai and Panchkula;

Expected rentals of INR 3,300 crores once the 307 MW is fully operational.

iii. FY24-29: Revenue CAGR of 34%

Expected revenue in FY29 of Rs 3000 (real estate)+ Rs 3300 (data center rentals) would implies revenue rowing Rs 6300 cr in FY29 from Rs 1483 cr in FY24 at a CAGR of 34%. The Rs 6,300 cr of revenue does include any other revenue from other parts of its residential and commercial businesses.

8. PAT growth of 82% & revenue growth of 48% in Q1-25 at a PE of 58

9. So Wait and Watch

If I hold the stock then one may continue holding on to ANANTRAJ

ANANTRAJ has a track record of delivering strong performance with a FY20-24 PAT CAGR of 189% & Revenue CAGR of 78%. The historic performance was continued in FY24 and followed up in Q1-25 with an extremely strong performance.

FY24 PAT: I am very pleased to share that this is the company's best profit so far, which we have achieved over the last 15 years.

The outlook of ANANTRAJ growing 4X+ form a Rs 1483 cr business to a Rs 6300 cr business by FY29 is a strong reason to continue with it. Q1-25 execution shows that its moving in the right direction to achieve FY29 targets.

10. Join the ride

If I am looking to enter ANANTRAJ then

ANANTRAJ has delivered PAT growth of 82% with revenue growth of 48% in Q1-25 at a PE of 58 which makes the valuations acceptable in the short term.

The outlook of ANANTRAJ to deliver revenue CAGR of 34%+ for FY24-29 at a PE of 58 makes the valuations quite acceptable over the longer term

ANANTRAJ is a story which will develop over the next 5 years and one needs to keep a close watch on the execution as the margin of safety is limited at a PE of 58.

Since ANANTRAJ is a longer term story one can build positions over a period of time.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer