Anand Rathi Wealth: 34% PAT growth & 33% revenue growth in 9M-25 at a PE of 58

Guidance of 30%+ PAT & Revenue growth in FY25. ANANDRATHI is a sustainable 20-25% growth business. Tailwinds of rising HNI population seeking wealth services leading strong inflows into equities.

1. Why is ANANDRATHI interesting?

anandrathiwealth.in | NSE: ANANDRATHI

ANANDRATHI is performing strongly, achieving consistent PAT growth of over 30%. This success is fueled by India’s emergence as the fastest-growing economy in FY25, which has led to an increasing number of high-net-worth individuals (HNIs) looking for strategic wealth creation approaches. Additionally, equity markets are seeing record-high inflows, with new investments rising month after month.2. India’s leading wealth firms, catering to high & ultra-high net-worth individuals

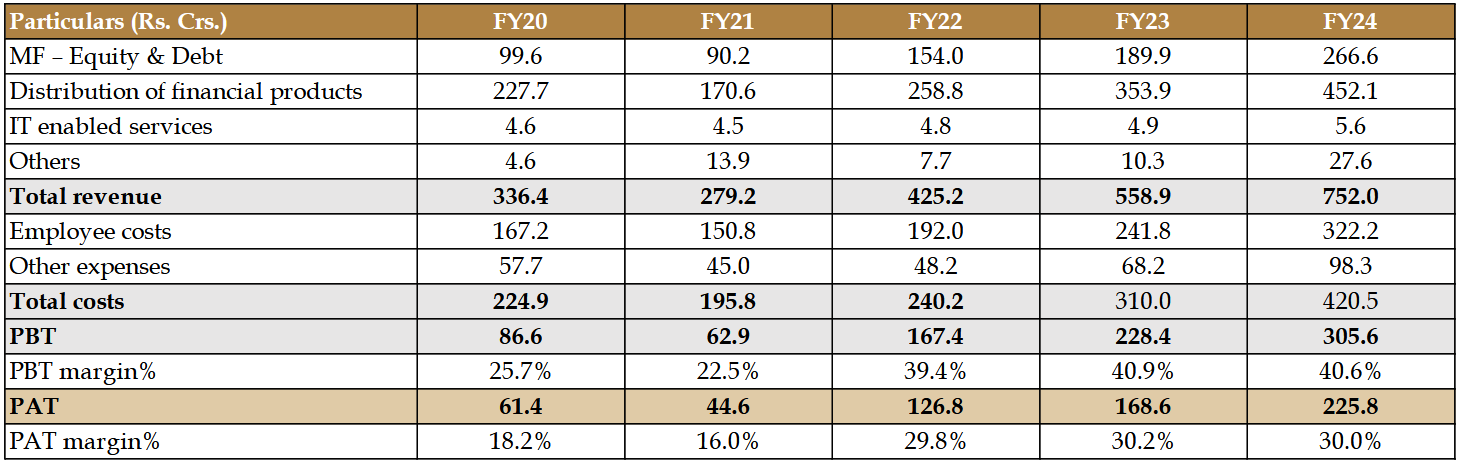

3. FY20-24: PAT CAGR of 38% & Revenue CAGR of 22%

4. Strong FY-24: PAT up 34% & Revenue up 35%

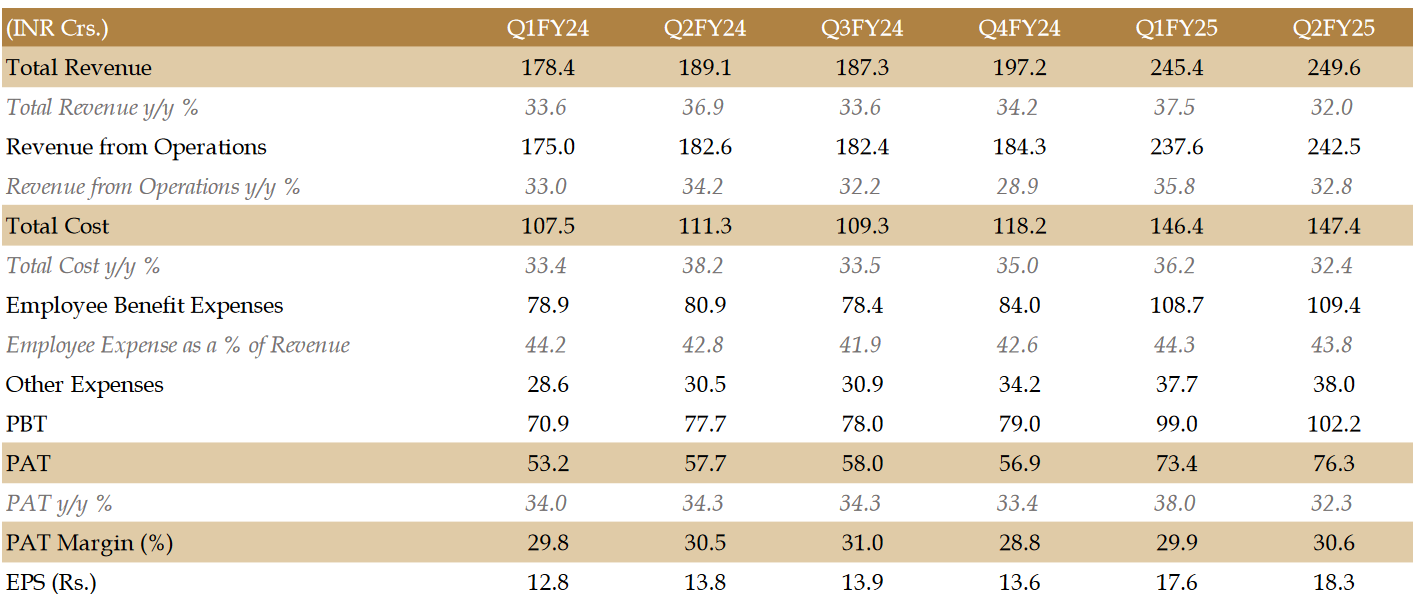

5. Strong Q3-25: PAT up 34% & Revenue up 33%

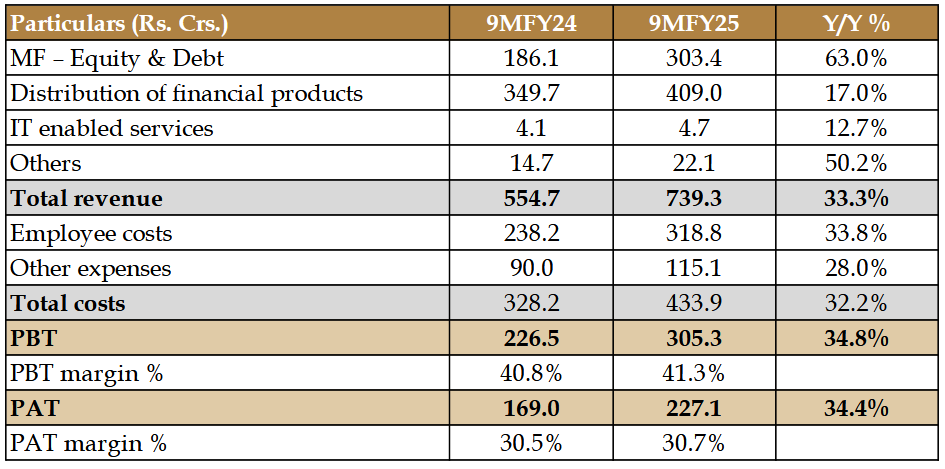

6. Strong 9M-25: PAT up 34% & Revenue up 33%

7. Strong return ratios

8. FY25: PAT growth of 31% & Revenue growth of 30%

9. PAT growth of 34% & Revenue growth of 33% for 9M-25 at a PE of 58

10. Hold?

If I hold the stock then one may continue holding on to ANANDRATHI

9M-25 performance indicates that ANANDRATHI is on track to deliver on its FY25 guidance. There is a possibility that ANANDRATHI may outperform its guidance for FY25.

The underlying business momentum and execution in ANANDRATHI is strong. The trend has continued in Q3-25 which has delivered an AUM growth of 39%

ANANDRATHI is the middle of a strong run in the business which has continued into Q3-25 where PAT has grown at 30%+ YoY for the last 7 quarters. One should continue with ANANDRATHI as long as the strong run continues.

One should hold on as long as the management holds on to its promise of 20-25% growth business with a 30% PAT margin. Its not easy to find a 20-25% growth business with a 30% PAT margin at a scale.

We believe that our business holds inherent growth potential of 20-25%, which we expect to sustain for many years.

The outlook for ANANDRATHI is supported by strong tailwinds given the fact that India is expected to be the fastest growing economy in the world in FY25

prospects are positive, supported by the rising HNI population who are seeking a strategic approach to wealth creation.

consistent inflows into the equity markets, with new investments hitting record highs month-on-month

11. Buy?

If I am looking to enter ANANDRATHI then

ANANDRATHI has delivered a strong 9M-25 with PAT growth of 34% & revenue growth of 33% at a PE of 57 which makes the valuations quite rich in the short term.

Guidance of 30% PAT growth in FY25 by ANANDRATHI is already discounted in the price at a PE of 57

Guidance of ANANDRATHI being a sustainable 20-25% growth business over the longer term at a PE of 58 provides an opportunity over the longer term.

At a PE of 58 the margin of safety is limited in ANANDRATHI, one not so strong quarter and the stock may start looking quite expensive.

If the trend of PAT CAGR of 38% for 20-24 continues then there is value in ANANDRATHI over the longer term even at current PE of 58.

Previous coverage on ANANDRATHI

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer