Anand Rathi Q4 FY26: Outperformance & Conservative Guidance

Anand Rathi Wealth Q4 FY26 earnings beat guidance with strong PAT and AUM growth, but FY27 guidance stays conservative—raising questions on premium valuation.

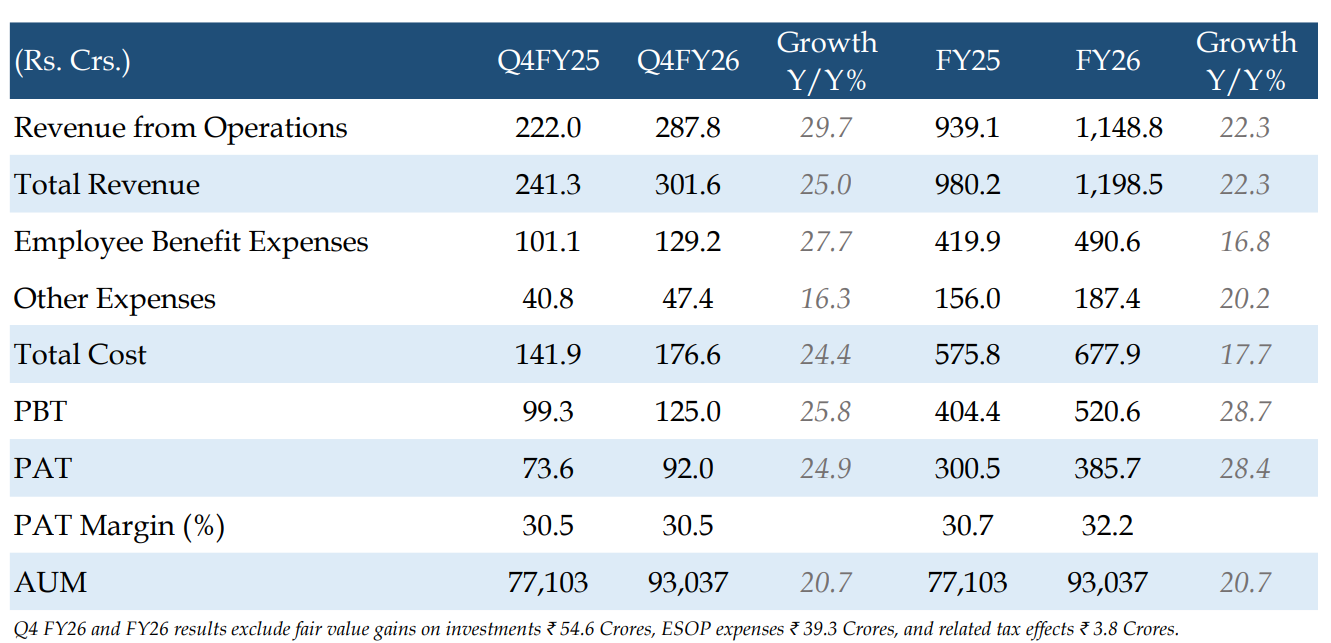

Financial Highlights

Anand Rathi Wealth presents strong financial momentum based on FY26 — in a year of macro weakness

Highly impressive, industry-leading Return on Equity (ROE) of 46.74% for FY26.

Delivered greater than 20% Profit After Tax (PAT) growth for 18 consecutive quarters, which management notes is a rarity among NSE 500 companies.

To reward shareholders, the board approved a 1:1 bonus share issuance and a final dividend of 7 rupees per share.

High Earnings Predictability and Future Guidance

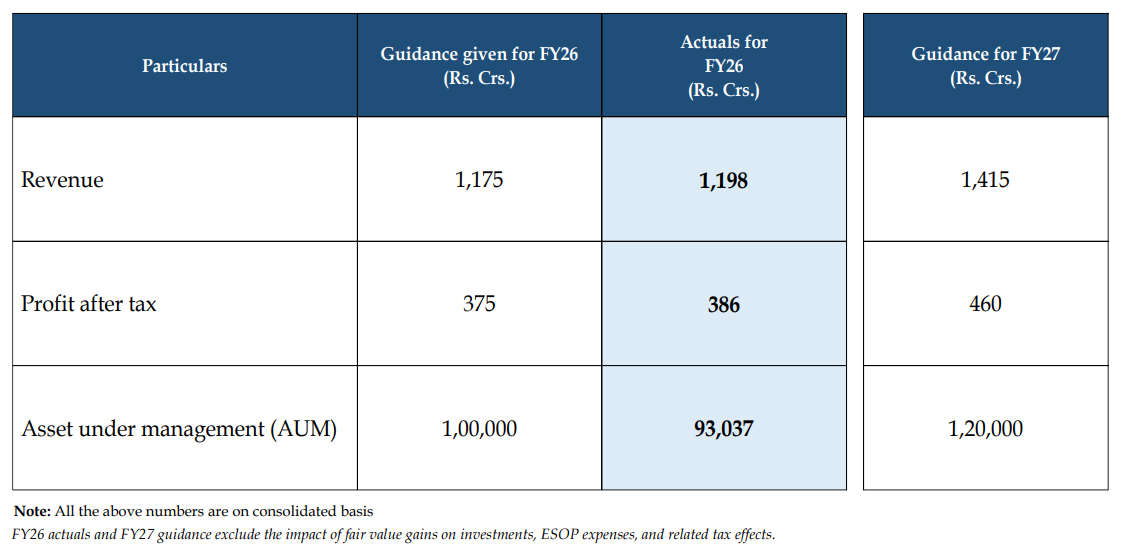

Even after out-performing against the FY26 guidance, management operates on a philosophy to “under commit and over deliver”.

FY27 PAT of ₹460 Cr PAT represents an 19% growth over actual FY26 figures — nothing extra-ordinary

Management clarified that it aligns with their historical 20-25% long-term growth trajectory when measured against previous base expectations.

A massive advantage for revenue visibility is that 99% of the firm’s business comes from structured products with rollover options, allowing the company to plan its financials as far ahead as 2031.

The miss on AUM was compensated by the outperformance on revenue & PAT

Business “Moats” and Operational Resilience

Insulation from RM Churn: A major risk in wealth management is Relationship Managers (RMs) leaving and taking clients with them.

However, when seven RMs left the firm recently, Anand Rathi successfully retained 81% of those departing managers’ client assets.

Overall client attrition is exceptionally low at just 0.54% of AUM.

In-house Talent Pipeline: Instead of paying exorbitant salaries to poach lateral hires from competitors, the company heavily relies on training raw talent.

In FY26 78% of their 45 new RMs were trained internally from colleges.

Strictly Owned Branch Network: Future geographic expansion into tier-2 and tier-3 cities will be executed exclusively through company-owned branches managed by internally trained RMs returning to their hometowns, as management firmly rejects the franchise model.

The “Platinum” Growth Engine

A major catalyst for future growth is the firm’s “Platinum Segment,” which caters to ultra-high-net-worth clients with an average ticket size of ₹50 Cr and above.

This segment is highly lucrative, now making up almost 29% of the total business.

Management is seeing strong organic inbound interest from individuals with ₹400-500 Cr portfolios and expects the number of Platinum client families to more than double from 211 to between 450 and 500 over the next two years.

Premium Valuations for Premium Execution

Anand Rathi Wealth is trading at a market cap of ₹29,796.11 Cr against the FY27 PAT guidance of ₹460 Cr — FY27E P/E of 65x

These are premium valuations for a company promising 19% PAT growth

Even if we adjust for a conservative guidance and assume a 30% PAT growth in FY27 — Anand Rathi Wealth would still trade at FY27E P/E of 60x which remains at premium valuations

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer