Ami Organics Limited - Overpriced share

A good fast growing company, irrespective of the share price.

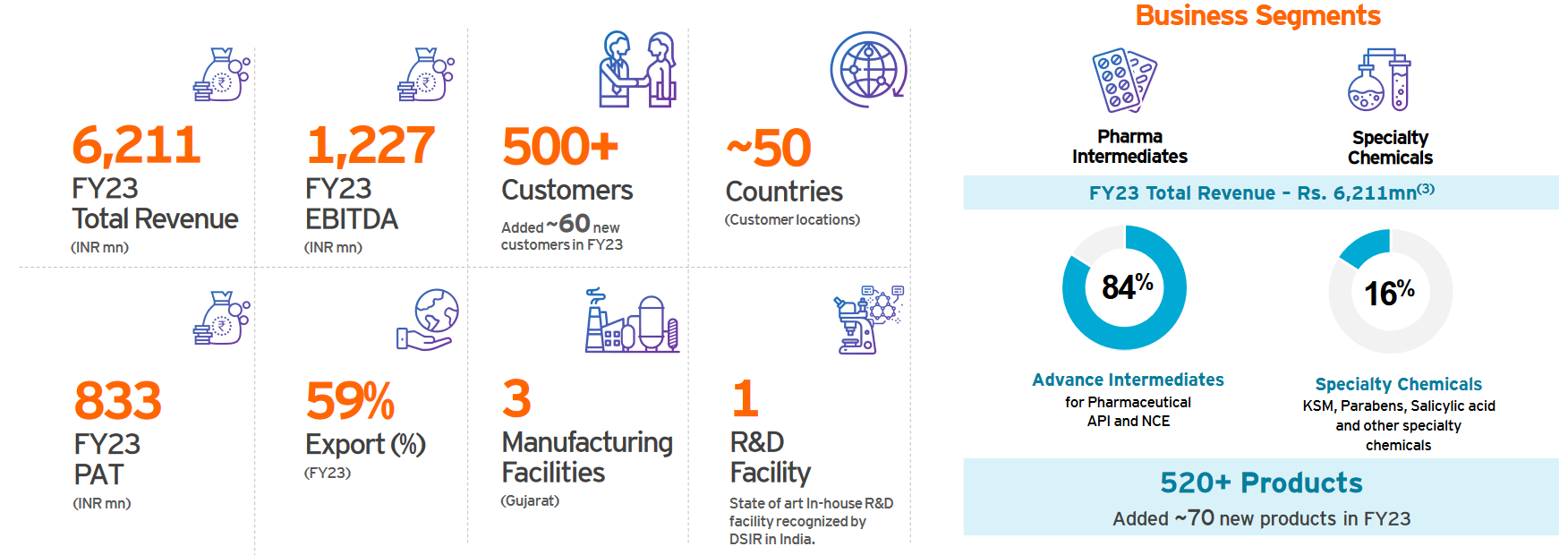

Company Overview

Ami Organics Ltd. is a globally integrated chemical intermediate manufacturing company located in Gujarat.

AMI Organics (AMI) is a research and development driven manufacturer of specialty chemicals with varied end usage and is focused on the development and manufacturing of advanced pharmaceutical intermediates (“Pharma Intermediates”) for regulated and generic active pharmaceutical ingredients (“APIs”) and New Chemical Entities (“NCE”) and key starting material for agrochemical and fine chemicals.

Share Details

NSE:AMIORG

Closing Price = 1,295.00 (19-Jun-23)

52 Week High = 528. Trading at 3% below 52 wk high.

52 Week Low = 825.35. Trading at 60% above 52 wk low.

P/E = 58

Market Cap = 4,773 cr ( ~$ 583 million)

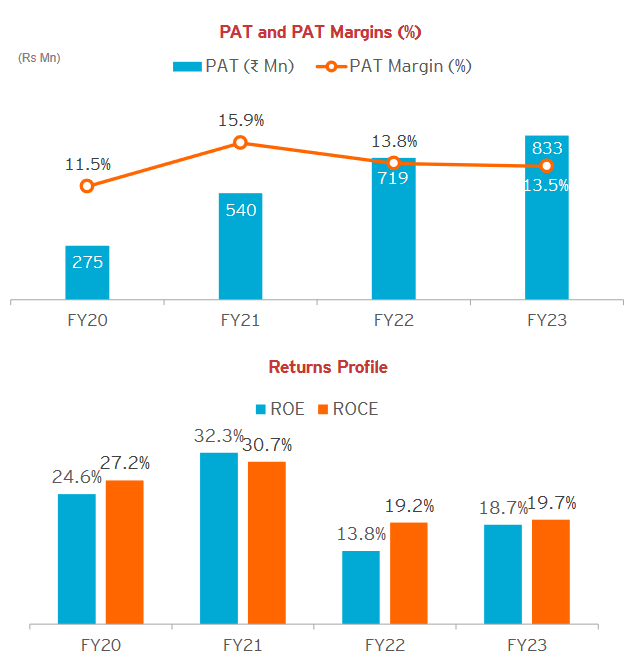

Quality: Returns on capital employed in cash

AMIORGANICS return ratios like ROE and ROCE are ok, but nothing exceptional. The cash conversion ratio is not exceptional.

Additionally, the return ratios have deteriorated in the last two years.

Growth

Growth numbers are good but the bottom line is lagging the the top line. The company is also unable to generate free cash flow performance in the last three financial years.

The margins and return ratios have deteriorated in the last two financial years.

A key business highlight in its Q4-23 investor presentation claimed that Ami Organics has started planning to set up 4.5 MW solar power plant in Gujarat. The correlation between solar and chemicals is unclear. Some may see it as a key business highlight, others may see it as key business red flag in terms of capital allocation and focus of the management.

The financial year 2023 has been very challenging on all fronts and I am happy that we have been able to deliver robust growth despite these challenges. Our full year total revenue grew by 19% YoY to Rs. 621cr.

Overall, I am confident of continuing the strong growth momentum in FY24.

Mr. Naresh Patel Executive Chairman and Managing Director

The top-line grew by 19% in FY23 and the management is confidently continuing the strong growth momentum in FY24. The growth momentum of 19% in FY23 continuing in FY24 does not sound very exciting

So What????

If I own the stock, I may keep it based on my historic returns, future return expectations, and availability of alternative stock ideas

If I don’t own the stock, I will make no efforts to own it at the current price levels. The past growth in top-line, bottom line and cash flows along with the 19% growth momentum indicated for FY24 does not inspire confidence to invest in a stock trading at a PE of 58.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades