Alkyl Amines Chemicals Ltd. - Expensive stock

A good company, but a guidance of 10-15% volume growth does not justify its price.

Company Overview

Established in 1979, Alkyl Amines Chemicals Ltd. (AACL) is a global supplier of aliphatic amines, specialty amines and amine derivatives to the pharmaceutical, agrochemical, water treatment, rubber chemical and a variety of industries.

AACL has around 640 employees and operates over 20 production plants over three manufacturing sites in Maharashtra and Gujarat.

It offers over 100 products and is a global leader in synthetic Acetonitrile, DMAHCL, Triethylamine, Diethylhydroxylamine and is sole global producer of many specialty amines.

Share Details

NSE:ALKYLAMINE

Closing Price = 2,611.95(23-Jun-23)

52 Week High = 3226.25. Trading at 19% below 52 wk high.

52 Week Low = 2146.1. Trading at 22% above 52 wk low.

P/E = 58

Market Cap = 13,325 cr ( ~$ 1.6 billion)

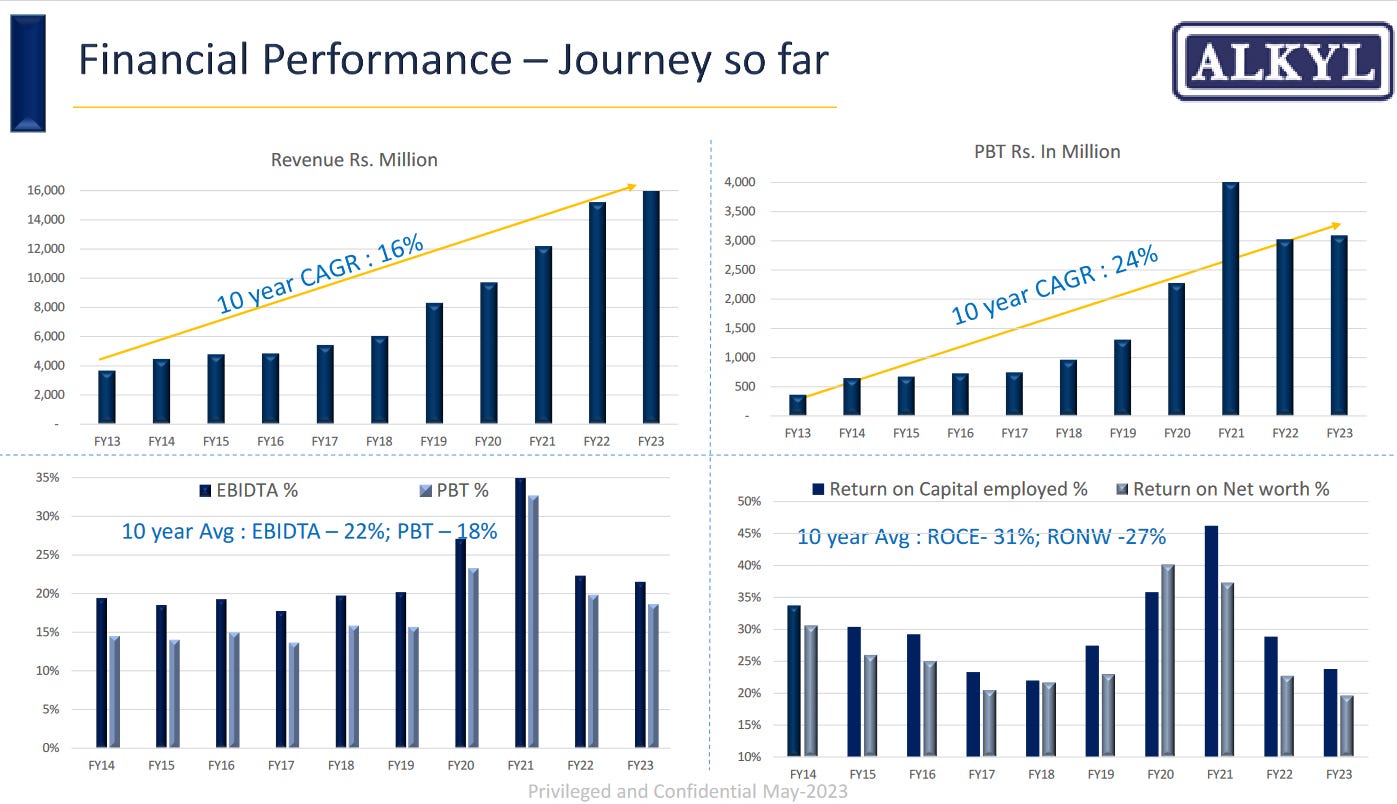

Quality: Returns on capital employed in cash

The return ratios are excellent and consistent since FY16 and is indicative of a high quality management running the company quite efficiently. Even if we exclude the Covid impact in FY20 and FY21, the return ratios have always been above 20%. Post Covid the PAT margin has improved as compared to the pre Covid margin, but it needs to be seen if the margin post Covid is sustainable.

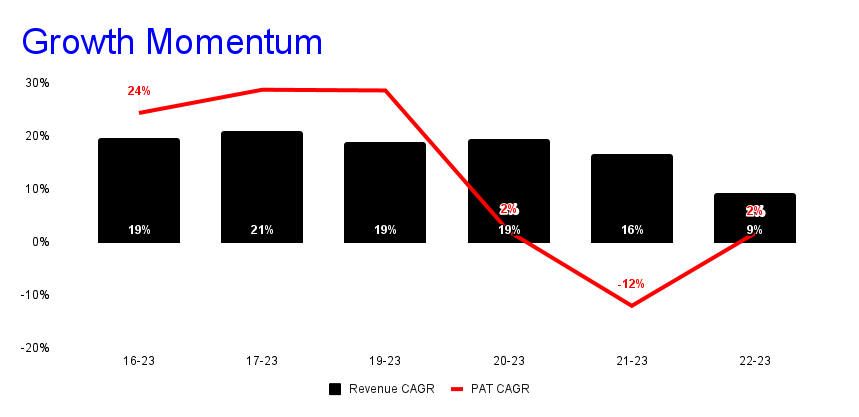

Growth

Both the top line and bottom line have grown consistently by 18% and 19% respectively. AACL hit its peak PAT at Rs 295 crore in FY21. It is yet to hit the peak PAT though top line was 35% higher in FY23 as compared to FY21.

The top line growth has been stable, but the same cannot be said about the bottom line.

Outlook

Looking at remarks made by the management during the Q4-23 earnings call, the company is continuing with is guidance of 10-15% volume growth in FY23 to FY24. While the company is hoping to do closer to 15% in volume growth, they are also expecting a better performance on the margin front though they they are hesitant to give a margin outlook.

In terms of volumes, in the last year we had predicted we will do between 10% and 15%. Unfortunately, it’s been at lower level at around 10% the volume growth. We are expecting next year to be a little better because things have stabilized and our customers are being a little more optimistic. And we hope to be able to do at the higher end of this 10% and 15% in volume growths.

The margin outlook, we normally do not speculate on our future margins because it’s very difficult. So, I wouldn’t speculate on the margin at all. But we are always hopeful that given that the raw material prices seem to be coming down, we would get some advantage in that.

So What????

If I own the stock, I may keep it based on my historic returns, future return expectations, and availability of alternative stock ideas. Its a good company and if I am sitting on historical returns then I may want to stay with it.

If I don’t own the stock, I may not want to enter it given that its very expensive at a PE of 58. For comparison Balaji Amines, (half of AACL in terms of market cap) is available at a PE of 23. Its very hard to justify a PE of 58 for a guidance of 15% top line volume growth in FY24.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades