Aditya Birla Money: PAT growth of 38% & Revenue growth of 40% in 9M-24 at PE of 18

BIRLAMONEY looks on track to deliver 30%+ PAT growth in FY24 which is in line with its historic PAT growth at a CAGR of 38%

1. Equity & derivatives broking services; Portfolio Management Services

stocksandsecurities.adityabirlacapital.com | NSE : BIRLAMONEY

Aditya Birla Money Ltd (ABML) is present in equity broking, commodity broking, depository services, PMS (portfolio management services) and distribution of products like mutual funds, insurance and loans of Aditya Birla group companies.

The revenue sources are well-diversified encompassing retail and institutional broking, fair value gains from wholesale debt market and portfolio management services.

Aditya Birla Capital Ltd, the holding company for the financial services business of the Aditya Birla Group, is the promoter of BIRLAMONEY.

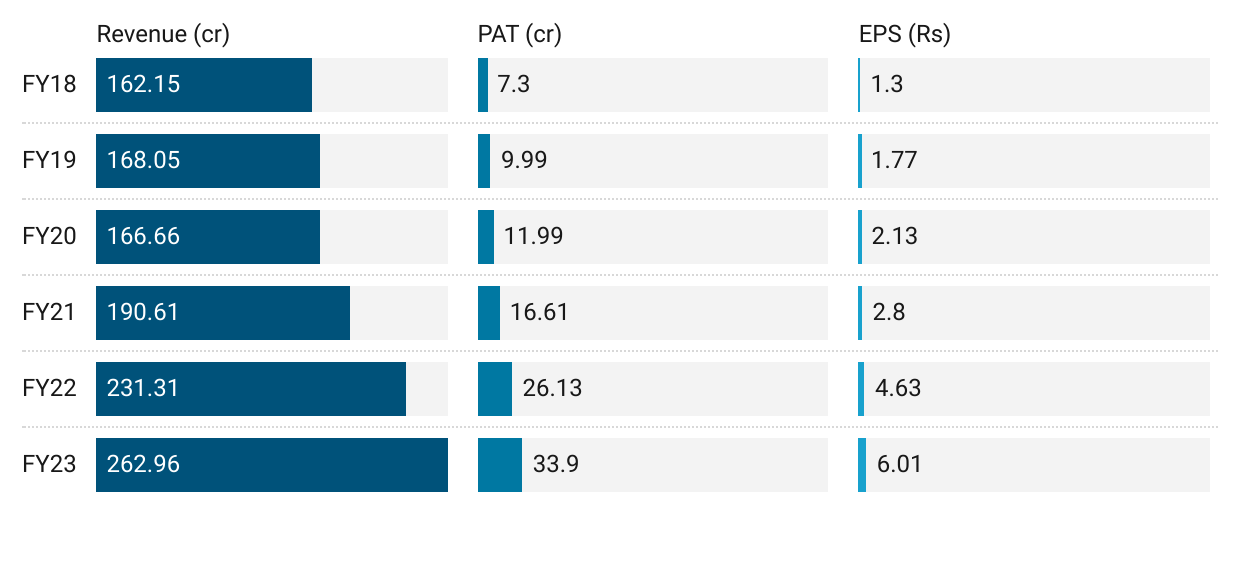

2. FY18-23: PAT CAGR = 36% and Revenue CAGR = 10%

3. Strong FY23: PAT up 30% and Revenue up 14% YoY

4. Strong H1-24: PAT up 20% and Revenue up 34% YoY

5. Strong Q3-24: PAT up 74% & Revenue up 5% YoY

PAT up 27% & Revenue up 51% QoQ

6. Strong 9M-24: PAT up 38% & Revenue up 40% YoY

7. Business metrics: Strong return ratios

8. Outlook: Expecting of continuation of FY18-23 trend

No management commentary is available on BIRLAMONEY

In the absence of management commentary one is expecting the continuation of the long term trend of PAT CAGR of 30%+ as delivered during FY18-23.

9. PAT growth of 38% & Revenue growth of 40% in 9M-24 at a PE of 18

10. So Wait and Watch

If I hold the stock then one may continue holding on to BIRLAMONEY

Based on H1-24 performance, BIRLAMONEY looks on track to deliver the strongest top-line and PAT in FY24

BIRLAMONEY is in the middle of a strong run. For all the 3 quarters of FY24, BIRLAMONEY has delivered QoQ and YoY growth in the top-line and PAT.

11. Or, join the ride

If I am looking to enter BIRLAMONEY then

BIRLAMONEY has delivered PAT growth of 38% & Revenue growth of 40% in 9M-24 at a PE of 18 which makes valuations quite reasonable.

Outlook for 30%+ PAT growth in FY24 based on 9M-24 performance at a PE of 18 makes the valuations quite reasonable.

In the absence of management commentary, the key question is will the momentum of FY24 carry into FY25. FY25 is less than 90 days away. If yes, then there exists potential for multi-bagger returns in this stock idea.

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action