Aavas Financiers: Huge runway for consistent and sustainable growth

Industry tailwinds driving 20-25% growth moving AAVAS on a trajectory of 15%-20% ROE while maintaining 5% spread

Company Overview

Aavas Financiers Ltd (AAVAS), formerly known as AU Housing Finance Ltd is a retail, affordable housing finance company. It serves the highly under penetrated and niche segments of low- and middle-income self-employed customers (65% of the book) in semi-urban and rural areas in India . Its product offerings include home loans for the purchase or construction of residential properties, and for the extension and repair of existing housing units.

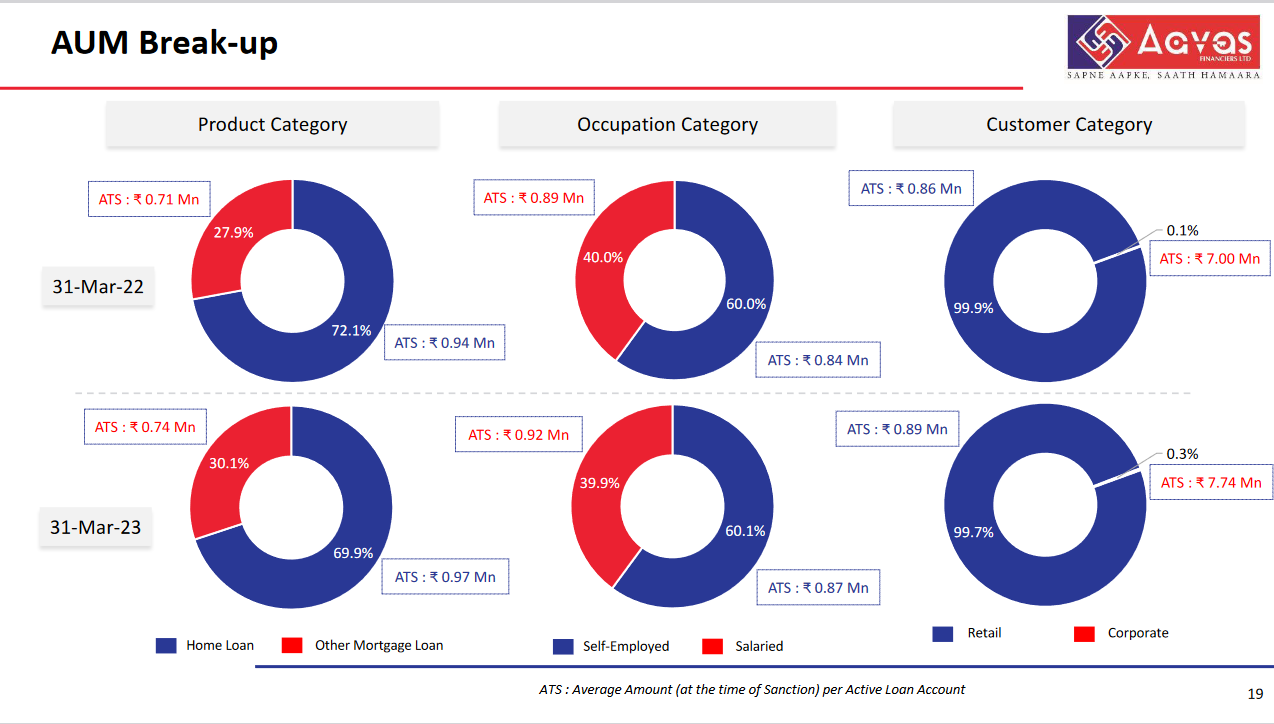

As a business strategy, we will remain at 70% to 75% home loan, 25% to 30% non-home loan book on a long-term basis

Share Details

NSE:AAVAS( aavas.in)

Quality: Returns on capital employed in cash

Since 2016 to 2023, in 7 years where we have seen Covid, we have seen liquidity crisis, where we have seen interest rate rising/falling, both scenario in that period, but across we maintained our spread at 5% plus.

Growth

We started in 2012, we are showing a disbursement growth of 27% and 23% is our 5 year AUM CAGR, even after 11 years of operations we are growing above 20% CAGR growth and this is across the markets which we have opened.

Growth Momentum

If you compare, let's say, the smaller companies which are in the size of INR 4,000 crores, INR 5,000 crores if you compare Aavas at the same journey in 2016 or 2017 in the time frame and then later on in the 2018 when we had a similar size, we were also growing 40% to 50% at that point of time. Now base has increased so with that higher base, obviously, will have that growth impact

Outlook

Strong industry tailwinds

What we see is that affordable housing as an industry is consistently growing at a very decent pace and the runway which is visible for us is very consistent and very sustainable

Strong guidance of 20-25% growth over the long term.

Branch size we see the next 10 year we don't see branch growth more than 10% every year. Topline will grow 20% to 25%, branches will grow 10%, headcount will grow 10% to 12% odd basically. All these matrixes will give us a better ROA and better ROE metrics Leverage is kicking in the - every year leverage is kicking basically

Growth will come with improved return ratios, FY23 ROE of 13% being guided to the 15-20% range.

Our opening net worth to closing net worth increased by 16%. In FY22 also and FY 23 also. So that shows the company now in the trajectory of 15% to 20% ROE business

Spread is the lending rate on loans minus the cost of funds for AAVAS. Spread being maintained at 5% indicates PAT margins will be stable.

now today we have Rs 14100 crores AUM still 5% spread is maintained that shows a long term liability and ALM management

So What????

If I currently hold the stock, I may continue holding it based on my past returns, expectations for future returns, and the availability of alternative stock ideas. AAVAS is on a 20-25% growth trajectory and one needs to keep riding it and ignore the temporary ups and downs.

If I don't currently own the stock, I may want to enter it at the current level.

Efficiently run lender with good return ratios

Industry tailwinds

Outlook for the future is strong

Available at a PE of around 29, the valuations are in line with the growth outlook.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades